Introduce a Dose of Optimism and Protection

Financial advisors and clients regularly discuss risk mitigation as it relates to financial threats. Life, health and property insurance are core elements of financial planning, yet a relatively common life occurrence isn’t broached nearly enough: divorce. Hoping for the best is insufficient, whether it relates to one’s own situation or those of your children.

According to the WSJ1, divorce rates are at a 40-year low. While the divorce rate dropped in 2017 to 16.1 per thousand marriages from 22.6 in 1979, aggregate statistics have no value if the person getting divorced is your daughter or son. Divorce settlements can compromise generational asset transfer and/or wealth creation, along with taking an emotional toll.

We frequently speak with parents concerned about the future possibility of a child’s divorce and are often asked what can be done to protect inherited wealth. Our recommendations typically focus on prenuptial agreements and dispositive provisions in estate planning documents.

Prenuptial Agreements

A prenuptial agreement offers a contractual roadmap concerning the property rights of each spouse in the event of a divorce or separation. In our view, prenuptial agreements are not just for the very rich and famous. Parents with concerns ought to consider the following:

A prenuptial agreement offers a contractual roadmap concerning the property rights of each spouse in the event of a divorce or separation. In our view, prenuptial agreements are not just for the very rich and famous. Parents with concerns ought to consider the following:

1. Review, if only in broad terms, your own wealth, financial and legacy goals and values with your children;

2. Discuss the benefits of a prenuptial agreement long before a child’s marriage is on the horizon. This can avoid “stigmatizing” a soon-to-be son or daughter-in-law as the wedding approaches; and

3. Prepare for questions and resistance with a sober, but firm rationale.

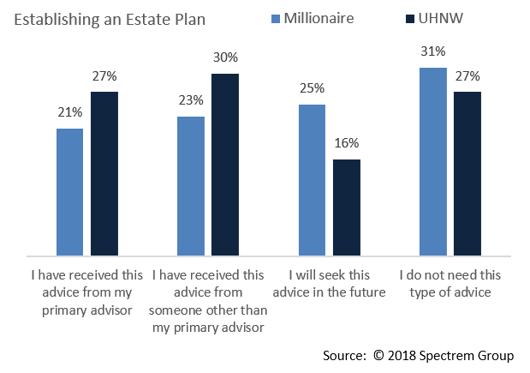

Estate Planning

Parents also need to understand how their estate plans are to be distributed to their children. Many estate plans pay out fully upon the death of the surviving spouse, or in sequential payments upon heirs reaching certain ages. These pay-out methods are fixed and, as such, cannot easily be changed.

A few estate planning options are worth considering as you think about what might work for your family:

1. Maintain assets in trust for your children’s entire lives and discuss why. This is what we’d call a “backdoor prenup”;

2. Add broader, more flexible discretionary distribution language; and

3. Name a friendly, knowledgeable Trustee.

Our Recommendations

We understand that these are not easy conversations. Nonetheless, assessing your options long before a pending marriage can ultimately help protect you and your children. We suggest at least thinking about the merits and tradeoffs associated with prenuptial agreements and estate plan distribution structures. Above all, we are happy to discuss your family’s unique circumstances.

How can we help you? Please contact:

Jim O’Neil, Managing Director, 617-338-0700 x775

[email protected]

www.www.appletonpartners.com