Insights & Observations

Economic, Public Policy, and Fed Developments

- After a spring marked by volatile economic data and a first half of 2024 plagued by uncertainty, July’s “goldilocks” economic data was followed at the end of the month by a surprisingly weak jobs report that raised recession fears and roiled markets.

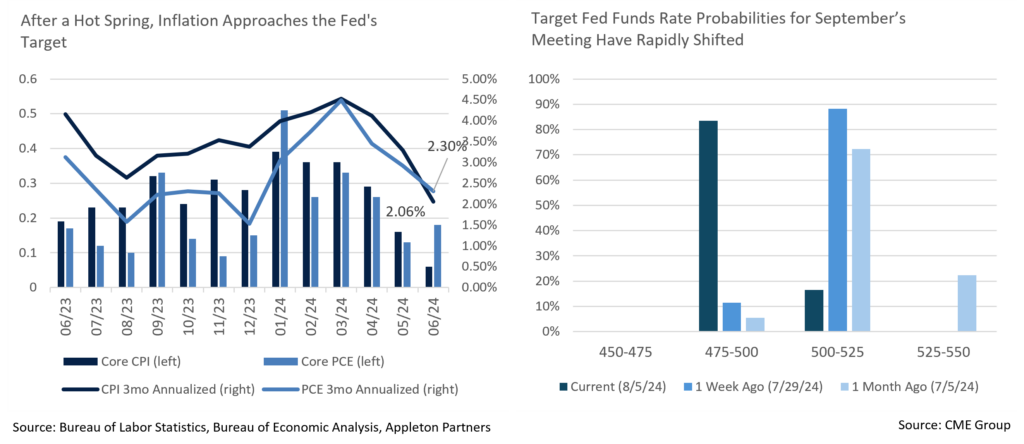

- July’s inflation reports, covering the month of June, were excellent. CPI could not have been much better, with a headline -0.1% drop and a core reading that barely rounded up to a below consensus +0.1%. While it’s taken longer than expected, the +0.2% monthly shelter costs were the lowest in years and annualized to the pre-pandemic norm of +3%. Looking at 3-month annualized CPI offers a better indicator of the current inflation picture than the trailing year, and June’s +2.06% is essentially at the Fed’s +2% target and has fallen sharply from +4.53% measured over the first three months of the year.

- The June PCE released at month-end was unremarkable, rounded up to an in-line +0.1% headline and +0.2% core inflation reading. The YoY core report came in a tenth higher than expected at +2.6%.

- The first estimate of annualized Q2 GDP was solid; +2.8% easily exceeded expectations of +2.0%. As expected, the growth rate was boosted by an inventory rebuild contribution that largely offset last quarter’s inventory drawdown. Personal consumption was solid at +2.3%, and final sales to domestic purchasers, and to private domestic purchasers, were both robust at +2.7% and +2.6%. Overall, it was a solid quarter although the “soft landing” investors have long sought was thrown into question at the end of July by weakening labor market conditions.

- The Conference Board’s June report on labor market confidence worsened unexpectedly and July’s release fell even further. Fuel was added to the fire on August 2nd when the Bureau of Labor Statistics reported that only 114,000 jobs were added in July, a sharp decline from June, and unemployment rose to 4.3%.

- US Treasuries surged in response as yields fell from 4.13% on July 31st to 3.79% as trading opened on August 5th. Equities plunged, ending an atypically long period without a major shock to risk assets. Volatility has reared its head once again, at least temporarily.

- The question now is the extent and speed of Fed Funds rate cuts, not when that cycle will begin. The latest futures data suggests 0.50% cuts in September and November, and another 0.25% in December, although a more positive ISM report on August 5th may somewhat ease fears and slow the pace of cuts.

- Politics is not taking a back seat to economic data. First, an assassination attempt on former President Trump shocked the nation. Then, bowing to growing party pressure, President Biden ended his campaign on July 21st, endorsing Vice President Kamala Harris to run in his place. This dramatic development set off a surge in Democratic enthusiasm and fundraising, altering the trajectory of a high stakes Presidential race.

- While the markets are still primarily focused on Trump as an inflation risk, neither candidate is likely to do much to stem longer term deficit issues, and there’s a risk this could eventually add to upward pressure on long yields regardless of who wins. For the moment though, the Treasury market is far more focused on economic data.

Equity News and Notes

A Look At The Markets

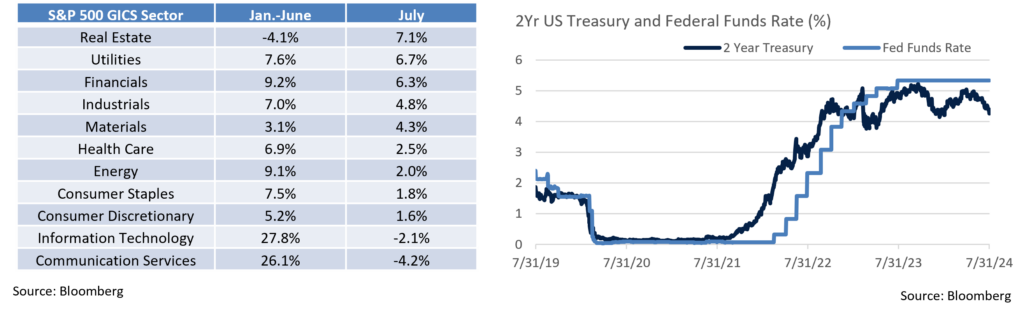

- Stocks were mostly higher in July, though a sharp rotation under the surface caused considerable dispersion between varying pockets of the market. The S&P 500 gained +1.1% to bring the YTD total return up to +16.7%, easily among the top 20% of YTD returns. The tech-heavy Nasdaq lost -0.8% on the month, while the DJIA gained +4.4%. Small caps led in July with the Russell 2000 gaining +10.1%, closing what had been a wide gap with large cap indices. Nine of the eleven sectors outperformed the broader market, led by rate-sensitive Real Estate (+7.1%) and Utilities (+6.7%), whereas Comm. Services (-4.2%) and Technology (-2.1%) fell.

- July’s big story was a rotation out of growth and momentum names following a weaker than expected June CPI report that raised expectations of a September rate cut. Small caps, value, and cyclical stocks all benefited from selling pressure on the crowded mega-cap tech trade. We have frequently highlighted the growing concentration risk at the top of the market, and an abrupt change in leadership was evident in the outperformance of the equal-weight S&P 500 (+4.4%) relative to its cap-weighted counterpart (+1.1%), the largest monthly margin since February 2021. Should rates continue to drop on falling inflation expectations, we would expect this trade to persist, but if yields fall on recession concerns, as has been the case in a turbulent start to August, economically sensitive small caps, cyclicals, and value stocks will struggle.

- In any walk of life, a handoff in power or leadership often comes with some instability. The same can be said for the stock market as the rotation out of “Magnificent 7” tech names has led to increased volatility. The S&P 500 experienced its first >2% down day in 356 trading days, its longest streak without a decline of that magnitude since 2007. Notably, the -2.3% drop on July 24th saw 164 of the S&P’s 500 names move higher on the day suggesting that internals were much stronger than the aggregate would imply. Where most of the year, critics were claiming weakness under the surface being masked by the “Magnificent 7,” recent vulnerability at the top could be masking strength under the surface.

- Earnings growth has continued to be a tailwind for stocks, despite a cautious tone surrounding the costs associated with AI. With 75% of the S&P 500 having reported for Q2, 78% have beaten earnings expectations by an average margin of 4.5%. While those rates are slightly below average, they are enough to bump the blended earnings growth rate up to +11.5%, well above the expectation of +8.9% to start the quarter.

- Unexpectedly weak labor market data once again raised recession fears at the very end of July and all eyes are now back on the economy and the Fed. Many believe the Fed has not cut rates soon enough to backstop a slowing economy, as can be illustrated in looking at the difference in 2Yr UST yields and the Fed Funds rate, as well as in the futures market where 50 bps cuts are now priced in for September and November. With no scheduled FOMC meeting in August, traders will look to Powell’s Jackson Hole speech in late August for more clues on the next move. Some have even called for an “emergency” intra-meeting cut, but we believe that such a move is unlikely as the Fed does not want to spark a panic, nor admit being wrong.

- Stock investors have always had to climb the “wall of worry”, the concept that markets tend to rise despite a laundry list of risk factors. The most recent list includes, but is not limited to, a Japanese yen carry trade unwind, US economic growth fears, a tight US election, Warren Buffet selling 50% of his Apple stake, heightened Middle East tensions, and valuation concerns. All have contributed to a risk-off sentiment to start August, historically a weak month. The VIX recently touched 65, its highest level since March 2020, and the S&P 500 sits more than 8% off its all-time high of mid-July. For now, this feels like a sell-off based on positioning rather than fundamentals, as overall credit, liquidity, and corporate earnings have been resilient. The patient investor is often rewarded for not selling into worry and we would lean into weakness as a buying opportunity at this point. A silver lining for balanced portfolios is that while the “bad news is bad” regime appears to be back, the stock/yield correlation is once again positive, and bonds are providing a valuable portfolio hedge.

From the Trading Desk

Municipal Markets

- July’s yield move had a steepening effect with the short end of the AAA municipal curve coming down more than longer maturities. The 2-year yield fell by 25bps with the 10-year moving down only 5bps, according to MMD.

- A move towards curve normalization gained ground as the spread between 2s and 10s began the month at 23bps and ended July at just 3bps. Weak labor market data shook up markets as August began, reinforcing expectations of multiple rate cuts beginning in September. We expect this process to drive down the front end of the curve.

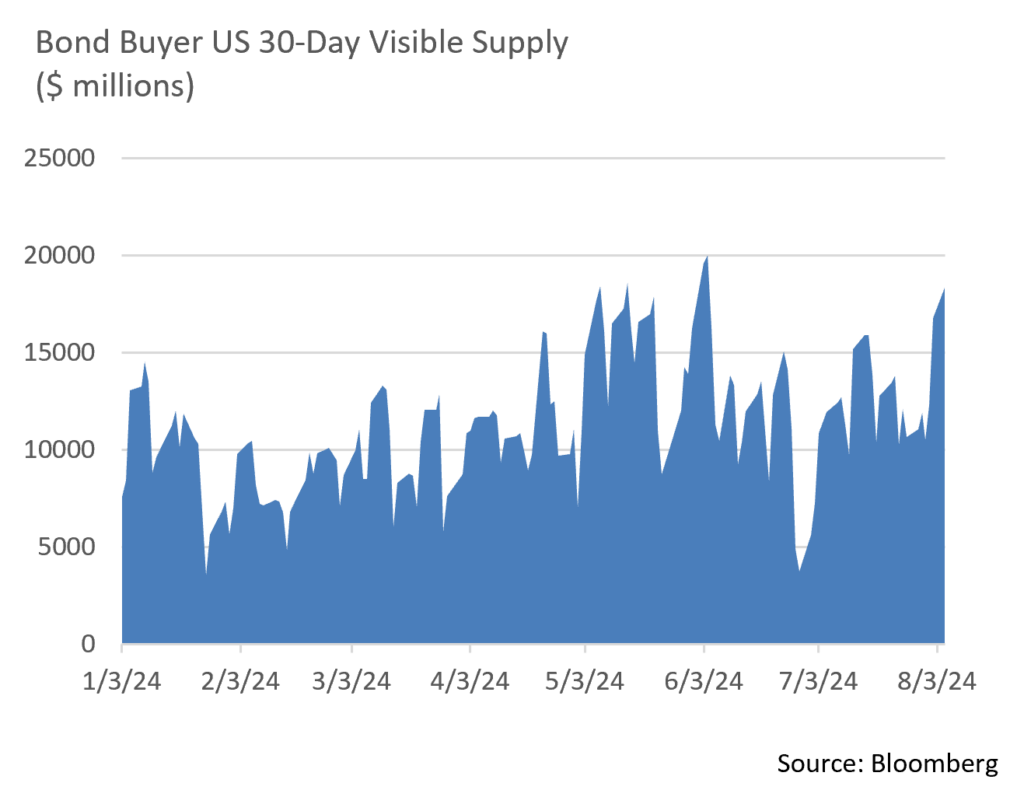

- Supply continues to dominate municipal technicals. According to Merrill Lynch, YTD issuance is up 33% through July relative to the same period of 2023. August has begun with heavy issuance and Bond Buyer 30-day visible supply is at a recent high of over $18 billion. We expect supply to be well received by investors, in part given that August’s reinvestment proceeds of $45 billion are well above July’s $36 billion.

- Recent market moves driven by a sudden decline in UST yields have caused the 10Yr AAA Muni/UST ratio to rise above 70%, a level that we feel offers value. To start the year, ratios were stubbornly stuck in a high 50% range and have spent the last several months in a 60% range. Over the longer term, we believe 10-year ratios are likely to settle in between 60% and 70%.

Corporate and Treasury Markets

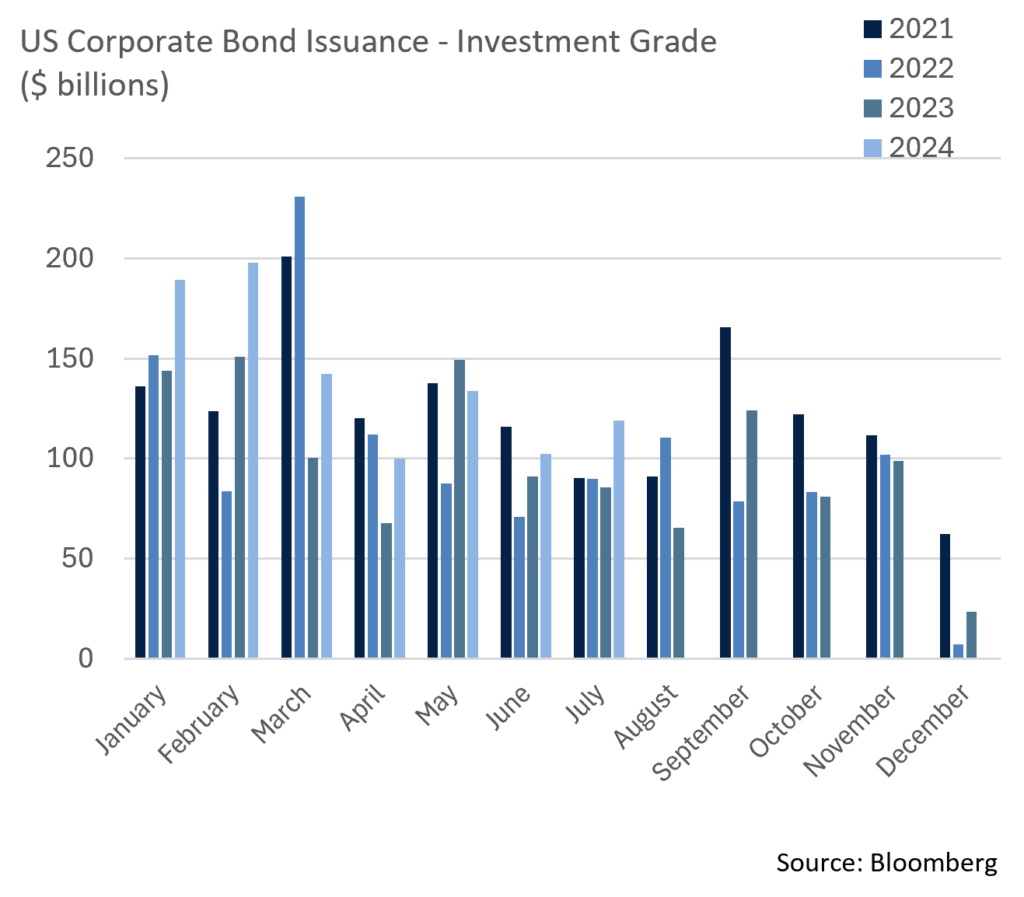

- Reception to the high volumes hitting the Investment Grade primary market remains very strong. The $118.9 billion of new debt that came in July fell just shy of July 2017’s record of $123 billion. Year-to-date new issue concessions (the added cost of issuing bonds) have been modest at 3.6bps and new deals have been an average of 3.7 times oversubscribed. July’s averages were even stronger with concessions of only 1.3bps and orderbooks oversubscribed by about 4 times.

- July’s spread movement was minimal and only produced 1bp of widening. The 94bps month-ending OAS was just 2bps higher than the YTD average of 92bps. An incredibly strong supply/demand metric continues to keep spreads stable, with the range limited to 20bps over the course of the year.

- Spread movement and risk sentiment are typically dictated by economic news and the Federal Reserve’s short term rate policy. Weak labor market reports prompted a rapid rally in UST prices and an equity market sell-off as the calendar turned to August, although IG credit has thus far held up well. Spreads widened initially by about 10bps before falling back several basis points.

- According to Lipper data, Short and Intermediate Investment Grade funds recorded ~+$3.57 billion in net inflows on the month and High Yield bond funds received ~+$4.48 billion in inflows, offering a further indication of healthy demand for credit. The “risk-off” move referenced above is testing investor sentiment, although we are not expecting IG Credit demand to materially decline.

- Supply may become challenging longer term for the US Treasury markets as $16.7 trillion of new securities have been issued in 2024 through the end of July, a 43.2% YoY increase. July’s $2.6 trillion was the largest month of issuance this year and just over $2 trillion of that was in short maturity Bills.

Financial Planning Perspectives

Update on SECURE Act Final Regulations

The IRS issued its initial Proposed Regulations regarding the SECURE Act’s operating provisions in early 2022. It included a big surprise – not only would “Non-Designated Eligible Beneficiaries” be subject to the 10-Year Distribution Rule, but if the original account owner had been receiving Required Minimum Distributions (RMDs) prior to their death, the designated beneficiary(ies) would also need to take annual RMD throughout the 10-year period. Beneficiaries are also required to fully distribute the account by the end of the 10th year.

New final regulations were issued on July 18, 2024, with the IRS confirming the above noted requirement for Non-Designated Beneficiaries to take RMDs.

It should be noted that due to the confusion caused by new distribution rules, the IRS has waived all RMDs for 2021-2024 and the IRS has confirmed that there will be no penalty and no requirement to make up the missed distributions. RMDs from inherited IRAs where the owner was already in RMD mode will be required to be taken starting in 2025.

Beyond confirming post-death RMD rules, the Final Regulations offered additional regulatory guidance concerning specific circumstances in which the new rules for Eligible and Non-Eligible Designated Beneficiaries apply.

According to a recent post on Kitces blog, these include:

- New rules for handling undistributed RMDs in the year of an account owner’s death.

- A new “Hypothetical RMD” rule for surviving spouses who initially elect to use the 10-Year Rule but later choose to roll-over or treat the inherited IRA as their own.

- Specification that when a plan participant has 100% of their plan balance in a Designated Roth account, Non-Eligible Designated Beneficiaries are not required to take annual RMDs during the 10-Year Rule period.

- Clarification of the requirements for successor beneficiaries who, depending on circumstances, may need to begin a new 10-year period after which the account must be fully distributed, or finish out the original beneficiaries’ 10-year period.

- New definitions of which beneficiaries of a “See-Through Trust” are also considered beneficiaries of the retirement account(s) and which definitions may be disregarded for retirement account purposes.

- A new rule providing that when a See-Through Trust is divided into separate trusts for each beneficiary upon the death of the retirement account owner, the RMD rules will be applied individually for each trust beneficiary rather than uniformly across all beneficiaries based on the beneficiary with the shortest required distribution timeline.

- Clarification that retirement accounts, including IRAs, that own annuity and non-annuity assets, can aggregate those assets for the purposes of calculating the participants’ RMD, and the payments from the annuity can count against the total RMD for both annuity and non-annuity assets.

In addition to the Final Regulations issued regarding the original SECURE Act, the IRS also released a new set of Proposed Regulations addressing questions concerning the SECURE Act 2.0. Points of note include:

- A widely applauded increase in the RMD age to 73.

- Clarification that surviving spouses of retirement account owners can elect to be treated as the decedent for RMD purposes.

We recognize that new and revised regulations introduce complexity to tax and estate planning, particularly after the death of a retirement account owner. That makes understanding these provisions all the more important, particularly given their potential implications. Your Portfolio Manager is here to help you work through individual circumstances and can also coordinate with your other trusted advisors.

Source: Untangling The IRS’s New Finalized (And Proposed) Regulations On RMDs: The 10-Year Rule, Trust Beneficiaries, Spousal Beneficiaries, Annuities, And More! Kitces.com LLC

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.