Insights and Observations

Economic, Public Policy, and Fed Developments

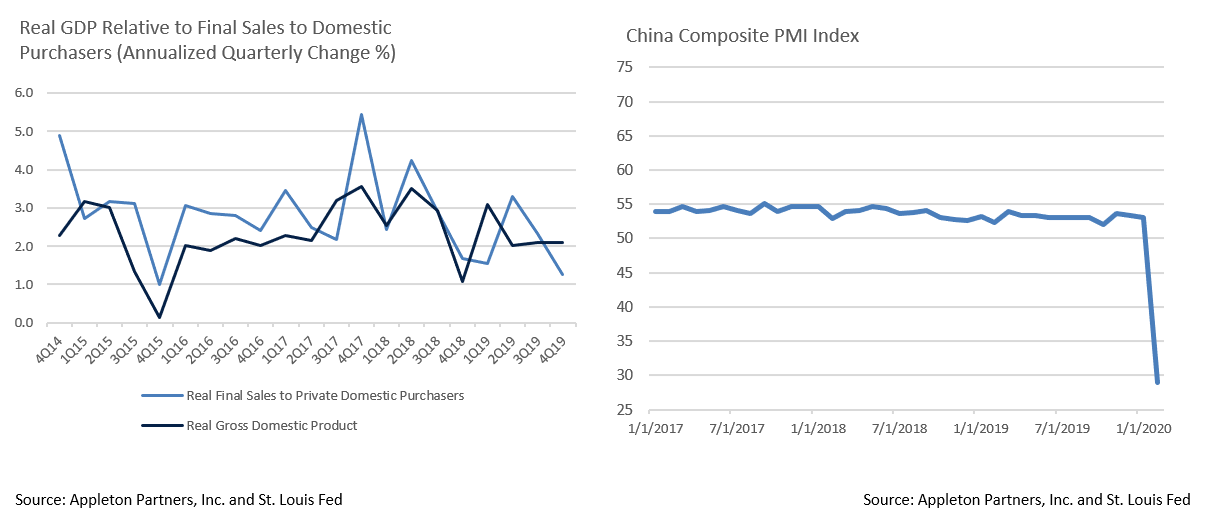

- Coronavirus fears began permeating the market in earnest in February, as reports of European supply chain disruption caused investor skittishness early in the month. Fear came to a head over the weekend of February 22nd, however, when a sudden uptick of cases in Italy, South Korea, and Iran compromised hopes for Chinese containment. Equities skidded into correction over the following week while Treasuries set record lows, with the 10Yr Treasury touching 0.909% midday on March 3rd before closing at 1.00%. Abysmal Chinese PMIs (the composite dropped to 28.9), the lowest on record (readings below 50 indicate contraction) provided compelling evidence of economic pain. This points to a profoundly negative impact on business supply chains and consumer demand due to necessary virus containment measures.

- This comes at a challenging time for the US economy, as evidence suggests consumer demand had already begun to lag before Coronavirus gripped the markets. Retail sales weakness continues, and while technically the headline 0.3% met expectations, the control group (a component of GDP) was flat, with December revised down three tenths to 0.2% and November revised down a tenth to -0.2%.

- Meanwhile, the PCE deflator, an important personal consumption indicator, dropped from an already sluggish 1.3% to 1.2%. Should Q1 consumption fall significantly it would be off an already weakening base, leading to a critical forward-looking question of whether Coronavirus fears are merely delaying economic activity or displacing it entirely. The bond market is pointing to the latter, while equity bulls are counting on the former.

- The Fed responded to the sharp repricing of Coronavirus risk on March 3rd with an unusual between-meeting 50 basis point rate cut, the first time they had adjusted rate policy between meetings since the Financial Crisis in 2008. This failed to sooth the markets, and further rate action is likely. Futures markets quickly priced in most of an additional rate cut at March’s meeting.

- In other Fed news, Trump Fed nominee Judy Shelton testified to the Senate Banking Committee on the 13th. A highly partisan pick, Shelton was a Trump campaign advisor who has advocated for a return to a gold standard, and for the Fed slashing rates to weaken the dollar and discourage banks from depositing money at the Federal Reserve. Her testimony met bipartisan resistance, and Shelton’s nomination may ultimately be pulled. That would likely be well received by markets given the uncertainty her views introduce. If seated, she could become Trump’s pick to replace Jerome Powell at the end of his term.

Equity News and Notes

A Look at the Markets

- The S&P 500 suffered its worst week since 2008 to end February as growing concerns over the length and severity of the Coronavirus outbreak wiped out investor risk appetite. A recent commentary distributed to clients outlines thoughts from our equity team.

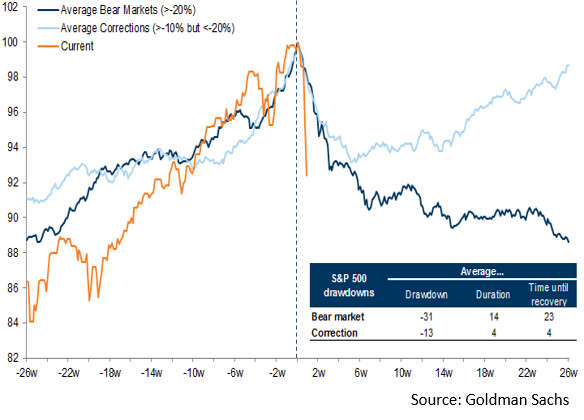

- At Appleton, we monitor a number of technical factors (RSI, moving averages, advance/decline lines, breadth), and sentiment indicators (VIX, put/call ratios) that, in our view, signal short-term oversold conditions similar to 2011 and 2015 declines. Volatility remains extremely high with sharp swings in both directions during the first week of March. Finding a bottom is more often than not an evolving process and stocks tend to retest their initial lows before ultimately recovering.

- Our last correction (Q4 2018), was one of the few cases where we saw a sharp V-shaped bottom. In this cycle our equity team expects more of a replay of 2011 and 2015, and see this period as a correction in the midst of a longer-term uptrend.

- Amidst the volatility, we are studying sector and style performance as this can provide valuable insight. Growth stocks have continued to outperform their value counterparts, particularly in the large-cap space, with the Russell 1000 Growth at -4.7% YTD vs the Russell 1000 Value at -11.6% as of March 3rd. The Technology sector, along with defensive bond-proxy sectors, have retained market leadership. Interestingly enough, mainland China stocks and emerging markets stocks have also outperformed, all encouraging signs.

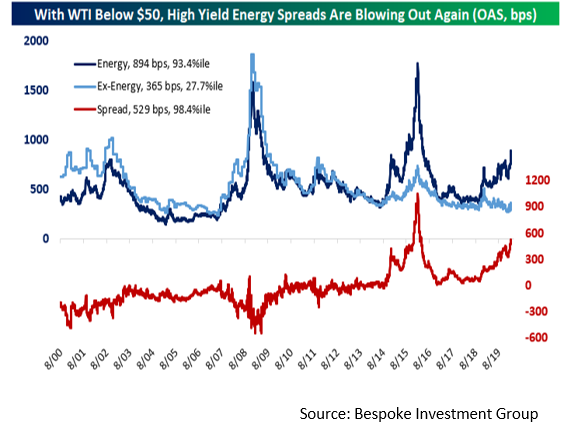

- On the downside, the Energy sector has been hardest hit, with the price of West Texas crude oil dropping more than 16% to less than $45 per barrel on demand concerns. While lower energy prices are a boon for US consumers, we are concerned about associated market stress. Credit spreads of energy companies, which make up roughly 11% of the high yield market, have widened considerably and the 10Yr Treasury hit 1% as we write on March 4th. Nonetheless, corporate credit spreads in aggregate have been better behaved, which is promising, and given a drop in benchmark rates, the cost of borrowing for companies remains low.

- The stock market swoon also coincided with what had appeared to be a growing prospect of Bernie Sanders winning the Democratic nomination. Super Tuesday’s Biden surge somewhat changed that narrative and it seems clear that equity markets prefer either a Trump re-election or a center-left Democratic presidency (Biden).

- As we move forward, we are studying the US consumer and corporate earnings given the importance of both factors to the bull narrative. Weekly jobless claims and consumer confidence reports will offer clues as to the impact of economic fears on consumer spending. A number of companies have announced that they will miss revenue targets amid the global uncertainty. While the consensus S&P 500 earnings growth projection for 2020 remains over 7% according to FactSet, this is certain to come down. How far is the question, although we continue to believe that an economic rebound is likely either in the second half of 2020 or early 2021.

- Lastly, in a somewhat surprising off-cycle move, the Fed cut the Fed Funds rate by 50 basis points. While we draw comfort from the willingness of global central banks to be highly accommodative, monetary policy alone is insufficient and a fiscal response could be needed. Ultimately, public health concerns need to be addressed and that takes time. Once the economy reaccelerates post-virus, the easy-money stance from the Fed should provide a boost, as it has during most of this bull run.

From the Trading Desk

Municipal Markets

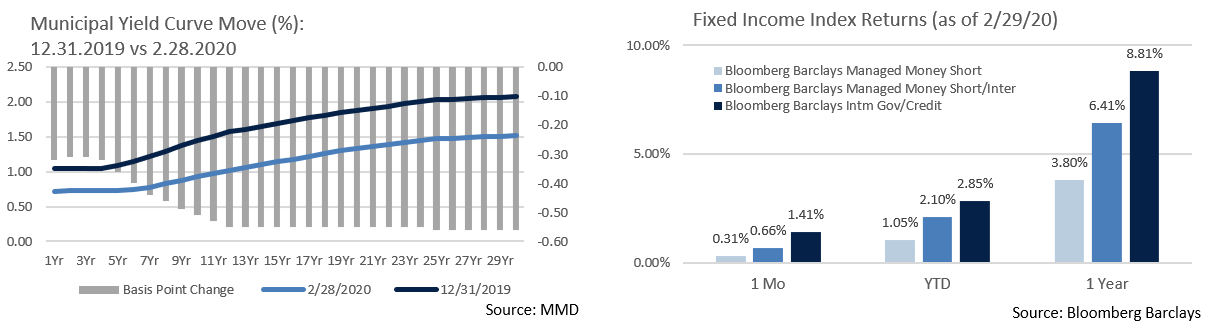

- The municipal curve is pushing lower and flatter on the heels of a pronounced Coronavirus influenced flight to quality trade. Over the month of February, 2-year AAA municipal yields fell by 10 basis points and 10-year AAA by 21 basis points. The 2-10-year spread ended the month at only 21 basis points versus 36 basis points at year-end 2019.

- Despite these low yields, which we discussed in “Operating in A Low Yield Environment,” mutual fund investors continue to see the value of municipals as a source of portfolio stability and tax-advantaged income. Tax-exempt funds have enjoyed another $23.6 billion in net new flows YTD in 2020, reaching 60 consecutive weeks of positive net inflows.

- Given this favorable backdrop, municipal performance has remained very strong. The Bloomberg Barclays Managed Money Short/Intermediate Index has returned 2.10% YTD through February.

- Taxable issuance has also been a major story, accounting for about 35% of total municipal issuance for the year. This is roughly 320% higher than the same period of 2019. Generally, the increase in taxable issuance reduces the supply of traditional tax-exempt offerings, a dynamic supportive of tax-exempt municipals. With yields driving lower, we anticipate additional large taxable issuance levels over the near-term, another positive technical factor.

Taxable Markets

- Corporate issuance closed January up 26% YoY and remained strong into February before extreme market volatility forced issuers to the sidelines. No deals came to market during the last week of February. The $86.67 billion of supply from earlier in the month reduced 2020 YoY volume by 8%. This has left pent up demand and issuers are standing by waiting for stability to return to the markets. Once a sense of normalcy returns, we expect as much as $50 billion of new issuance. Buyers are ready and we anticipate these offerings will be well received, thereby keeping a lid on corporates spreads.

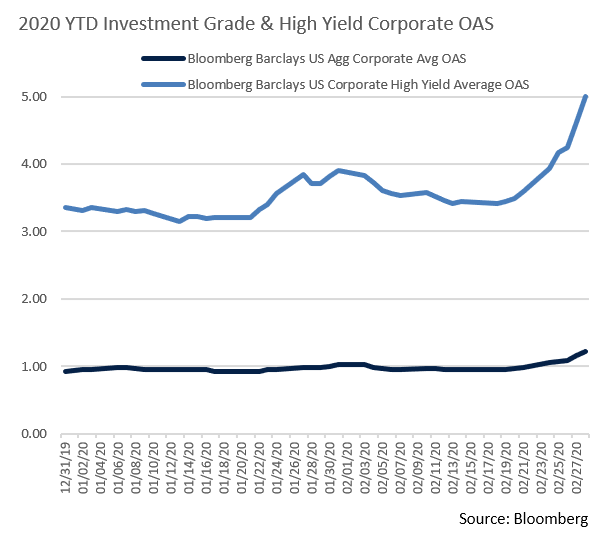

- Investment grade issues tightened through most of the month until the Coronavirus sell-off drove spreads in the other direction. Spreads ended the month at the widest levels since September of 2019, and the 8 basis points (7.4%) of widening from February 27-28 was the largest one day jump since the Financial Crisis. Notably, the stronger the credit quality the better pricing fared, as flight to quality moves tend to hit lower quality issues with far more vigor. High Yield option-adjusted spreads rose over the last week of February from 331 to 500 basis points, while CCC-rated corporate spreads (a quality rating we do not hold) exceeded 1,000 basis points over US Treasuries for the first time since August 2016. This market action speaks to our focus on more resilient, high quality, liquid corporate bonds.

Financial Planning Perspectives

Emotional Finance & Prudent Investor Behavior

No one knows what is going to happen in the financial markets on a day-to-day basis. The short-term direction and magnitude of market movements cannot be predicted with any reliability. Nonetheless, many investors try to beat the odds by market timing, often leading to chronic underperformance. So, during turbulent times what is one to do?

Work with your advisor to establish or reaffirm your personalized asset allocation. Appleton clients have already done this in consultation with our portfolio managers. Doing so helps establish goals, risk parameters and target allocations.

In investing, diversification refers to varying the nature and range of investments that make up an individual’s portfolio. Selecting investments with differing characteristics should help mitigate risk and create a more efficient overall portfolio. Three primary factors help us develop a personalized asset allocation strategy for clients:

1)Risk tolerance: your willingness and ability to tolerate the potential for loss

2)Objectives: your personal needs and goals

3)Time horizon: how long until you expect to begin drawing down funds and/or how long your assets need to last

Periodically reviewing your asset allocation strategy can be reassuring, particularly during times of market stress. This analysis factors in targeted exposure to stocks, bonds, cash and other asset classes, as well as more granular elements of your investment plan.

What should I do now?

Uncertainty can be difficult to tolerate. If extreme market volatility has you questioning whether you have the stomach to manage a market downturn, it may be prudent to reassess your appetite for risk. A good litmus test is to ask yourself “what is the maximum amount I am willing to temporarily lose in a market drawdown?”

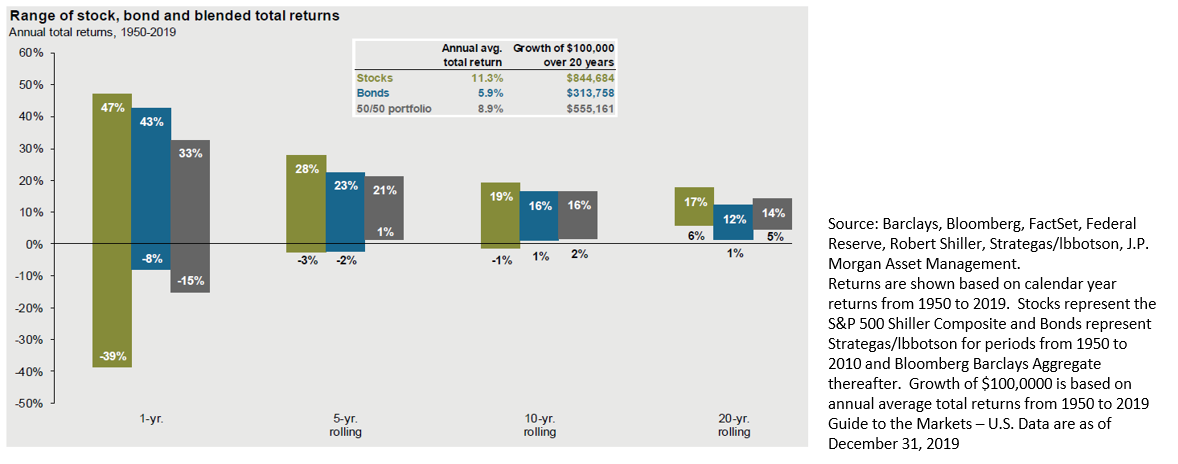

Provided your risk tolerance, objectives and time horizon have not changed, we urge you to stay the course. Trying to time the market as an investment strategy is almost always a losing proposition. Some of the best days for stocks have come in the first days of a market recovery. Staying invested long-term in an appropriate asset allocation has historically paid off. In fact, since 1950, there has never been a 10-year rolling period in which a 50/50 diversified portfolio of stocks and bonds has averaged less than +2% annual growth (see accompanying chart). But this assumes that assets remained fully invested. Pulling assets out at the wrong time can be detrimental to achieving your long-term goals.

If you have questions, please reach out to your portfolio manager.

For questions concerning our financial planning or wealth management services, please contact

Jim O’Neil, Managing Director, 617-338-0700 x775, [email protected]