Insights and Observations

Economic, Public Policy, and Fed Developments

- The US pandemic inflation debate has shifted from whether the Fed was right to expect transitory inflation, to what the Fed’s response to more persistent inflation will be as the reopening is delayed. The Fed met expectations on November 3rd by announcing tapering of asset purchases, leaving the timing of the initial Fed Funds rate hike as the remaining variable. While most market forecasts have generally pulled a hike forward to 2022, we believe the market may be getting ahead of itself, in part because it is unclear whether a rate hike would actually lower inflation.

- The Fed Funds Rate offers a means of tightening credit conditions when an overheating economy is running close to potential GDP and is still unable to keep up with demand. By increasing borrowing costs, demand can be slowed and rebalanced to output, cooling inflation. While “this time it’s different” arguments ought to be taken with a grain of salt, two current factors warrant consideration. First, the economy does not seem to be running anywhere near potential GDP. Output has barely returned to late 2019 levels and is plagued by short-term constraints. Second, after a protracted period of unprecedented US household savings, consumer spending is almost certainly being fueled by ready access to cash and not credit. We believe raising rates would be akin to pushing on a string and expect the Fed to focus on resetting expectations back to 2023.

- Although the prospect of Fed tapering while longer dated interest rates are rising makes some uneasy, we feel these concerns are misplaced. First, tapering of asset purchases still provides monetary stimulus, just at a slower pace. Second, Treasury issuance is expected to fall by an estimated $1 trillion over the next four quarters while the Fed tapers due to a shrinking budget deficit. And third, we believe changes in longer rates were driven by the Build Back Better Act, the Biden Administration’s massive “human infrastructure” plan, which in recent days has shrunk in size considerably. While as investors we would welcome higher rates and a steeper curve, rates are unlikely to rise materially in the near term.

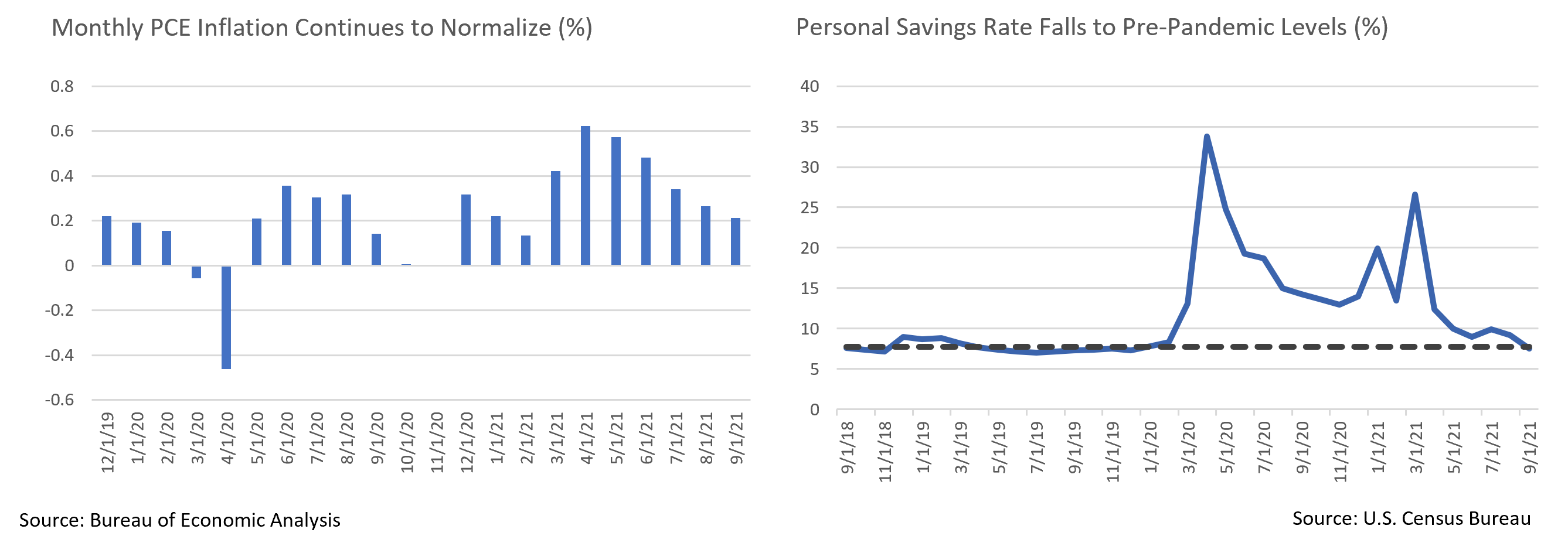

- Trailing monthly CPI and PCE inflation numbers continue to be eye-popping, and we expect pockets of inflation to persist as the COVID-19 situation evolves. However, inflation is slowing – while higher shelter-related weightings have added volatility to CPI, monthly PCE readings are falling and have returned to more normalized levels. September’s 0.21% monthly core PCE rate, annualized, is +2.56%, squarely within the Fed’s target range.

- September’s labor report produced a sizeable headline miss, although October’s pending report offers reasons for optimism. While we remain skeptical that enhanced unemployment is to blame for the decline in the labor participation rate, the US savings rate reverting to pre-pandemic norms may provide gradual pressure for workers to rejoin the workforce. The approval of COVID-19 vaccines for 5- to 11-year-old children may also help. And, while the 192k jobs created in September badly missed expectations, a supplemental household survey reported job growth slightly ahead of expectations. With seasonal factors related to earlier-than-normal education hiring also adding noise, September’s report could be setting up either an upward revision or an unexpectedly strong October report.

- Q3 GDP missed a “whisper number” of +5.7% and a Bloomberg median estimate of +2.6%, coming in at +2.0%. The details were bleak; a supply-driven decline in motor vehicle sales stripped 2.39 points off the headline number, and Final Sales to Domestic Purchasers, in normal times a good measure of core demand, was an anemic +1.0%. A positive contribution from Change in Private Inventories of 2.07 points was related to inventories being spent down at a slower rate, rather than stabilizing. Growth will remain hampered until further progress is made against COVID-19 globally.

Equity News and Notes

A Look at the Markets

- Following the worst month since the start of the pandemic, stocks rebounded sharply in October with the S&P 500 posting its best month since last November. The Index closed at an all-time high, gaining 7.0% to raise YTD total return to +24.0%. The Dow and Nasdaq also made fresh all-time highs and the Russell 2000 brushed up against its peak initially reached in March. Positive market breadth is evidenced by the NYSE cumulative advance/decline line, which also realized an all-time high to close the month.

- The S&P’s YTD gain marks only the 10th time since 1929 that the Index has increased by more than 20% at this point in the year. How have large cap stocks historically fared after hitting such lofty intra-year levels? Bespoke reports that in the prior nine occurrences the S&P 500 finished higher over the remainder of the year each time, posting a median gain of +5.9%.

- Last month we discussed a growing wall of worry facing investors. Much of October’s upside was driven by these headwinds somewhat abating. Congress agreed to kick the debt ceiling can down the road, the Evergrande real estate situation in China appears to have stabilized, supply chain disruptions showed signs of easing, and COVID-19 case counts are receding. The odds of a meaningful corporate tax increase also collapsed as Democrats negotiate the White House’s economic plan. We would not sound an “all-clear” on any of these matters but note that investors have seemingly priced in much of their concern.

- Q3 earnings season has also gotten off to a solid start. With over half of the S&P 500 reporting, 82% are beating earnings expectations, while 75% are beating on revenue, both above historical averages. Earnings are coming in 10.3% above estimates, which combined with a 82% beat rate, has lifted quarterly earnings growth to +36.6%. Though far short of the prior two quarters, this is well above the market’s +27.4% expectation (as of 9/30). Investors have been reassured by management commentary that demand remains robust in the face of what will hopefully be short-term supply chain issues. Mounting cost pressures, both on materials and labor, has raised concern about profit margins. While the net profit margin reported to date of 12.8% is down from Q2’s record 13.1%, it remains well above the 5-year average of 10.6%.

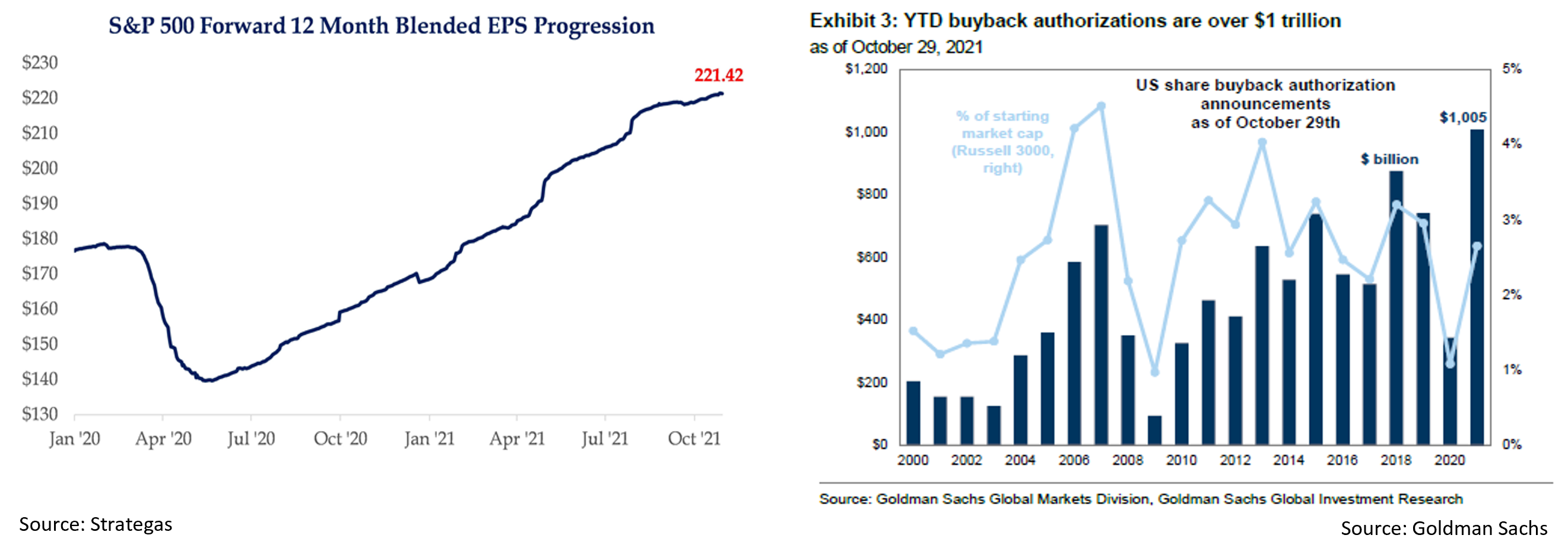

- Despite strong earnings, analysts have not been aggressively raising Q4 and 2022 projections. The forward 12-month S&P 500 earnings per share estimate is still trending up, although it has plateaued at about $221. Supply chain, inflation, and tax uncertainties linger, likely diminishing the outlook. With forward EPS stalling and current year earnings continuing to grow, next year’s growth estimates have receded to about +8.6%. These more modest expectations offer potential upside in our view, particularly if supply constraints recede.

- One reason for September’s weakness was the fact that corporations were in a buyback blackout period ahead of Q3 earnings season. Corporations have been the biggest net buyer of shares over the past decade with buybacks contributing 1 to 2% to EPS growth annually. A potential 1% buyback tax proposal is of concern, although we expect the impact would be modest. Buyback activity should accelerate as companies have already authorized a record $1 trillion in buybacks through the end of October. Companies were hesitant to go ahead with such plans earlier this year given an abundance of uncertainties, as evidenced by only $73 billion in net buybacks over the first half of 2021. We expect the gap between executed and authorized buybacks to close as companies deploy an estimated $2-3 trillion sitting on their balance sheets, a development that would provide a tailwind to the market.

From the Trading Desk

Municipal Markets

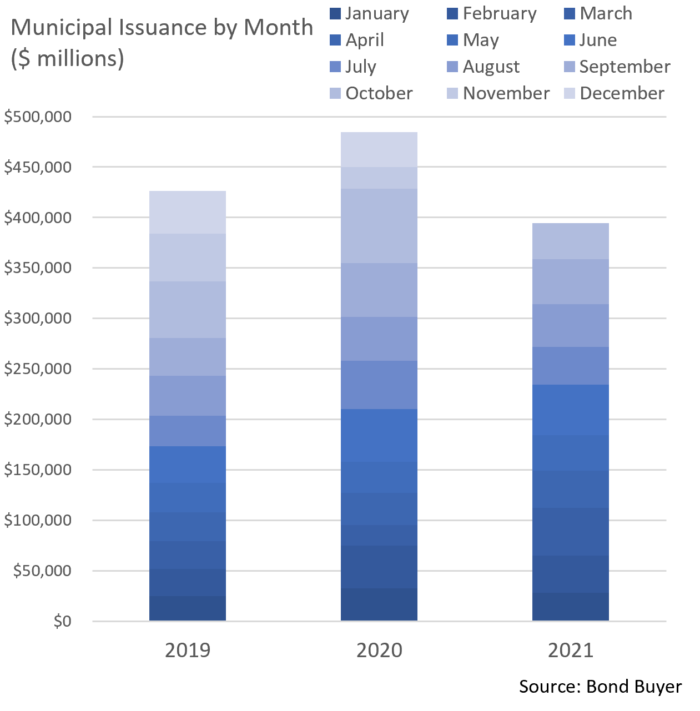

- It bears repeating that the municipal market’s supply and demand dynamics remain very favorable for bondholders. YTD new issuance currently sits at 92% of the same period of 2020, while prevailing estimates for 2021 total issuance will likely need to be revised downward. As for demand, mutual fund flows, a measure of retail buying strength, are up over $91 billion YTD. Despite recent moderation, 75 of 76 weeks have seen net fund inflows.

- As investors seek to put new money to work, high grade new issue names continue to be oversubscribed. This remains a challenge and we are actively working our dealer network to source attractive bonds in both the primary and secondary markets.

- Municipal yields edged higher over the month, following a corresponding move in Treasuries. While we could see some volatility through the end of the year, demand for municipals should keep yield moves muted. The spread on the AAA MMD curve between 2 and 10 years ended October at 96 bps, a level that benefits buyers who are selling shorter on the curve to buy longer dated issues. Our emphasis is on the 5 to 9-year part of the curve as it offers the greatest relative value given the increase in steepness vs. earlier this year. Over the course of 2021, a bear steepening trend has driven 10Yr yields up 50 bps, while the short end of the curve has only increased about 11 bps.

Corporate Bond Markets

- The investment grade credit market remained quite stable even as UST volatility ramped up over the course of the month. A good deal of that volatility was driven by Fed policy uncertainty, most notably the timing of tapering and possible future rate hikes.

- Investment grade credit spreads have rested in a very narrow range between YTD wide and tight levels. October began at 84 bps, before closing the month at 87 bps. The year began at 96 bps, with a YTD high of 100 bps reached on March 9th. Credit spreads are firmly anchored, and we feel they will trade in this band for the remainder of the year given corporate balance sheet strength and sustained investor demand.

- High grade supply surged in October as $120.2 billion of investment grade credit issuance set a monthly record. The market had no issues digesting the influx of new deals, although signs of investor fatigue are beginning to show. Order books were noticeably less heavily subscribed across most deals this month despite prices holding up well.

- We have also recently seen a reduction in refinancing as short UST rates tick higher and the need to do so diminishes. November and December tend to be quiet months and our expectations are for issuance to remain close to historical averages.

- A lot of attention was paid to the much-anticipated November 3rd announcement that Fed asset purchase tapering will begin later this month, a process that is likely to end by mid-2022. No mention of rate hike timing was given in the release or the press conference that followed.

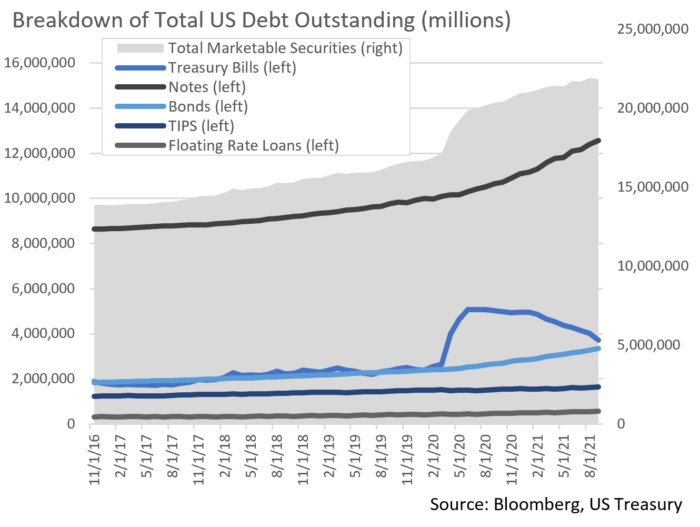

- Coincidentally, the US Treasury also recently announced that it will cut back on long-term debt sales as borrowing needs begin to slow along with reduced pandemic relief funding. The largest reductions in auction sizes will be in 7 and 20Yr maturities, which are falling by $3 and $4 billion respectively. Further reductions across all maturities will be revisited on a quarterly basis. These developments are bullish for USTs and leave room for excess capacity of non-coupon bearing Bills going forward as Congress revisits the debt ceiling.

Financial Planning Perspectives

Deal or No Deal? The Saga of the Build Back Better Act and the Infrastructure Investment and Jobs Act

Legislative Dealmaking Grinds On

It has been a tumultuous few months in Washington with Democratic infighting threatening the Biden domestic agenda, including the two major infrastructure and social spending bills. Not only has the price tag of the Build Back Better Act (“BBBA”) been significantly reduced, so have the means of paying for the social package. The $3.5 trillion bill passed by the House Ways and Means Committee on September 13th not only sought to raise the corporate tax rate from 21% to 26.5%, but it also proposed several other tax increases and restraints on high income and high wealth individuals:

It has been a tumultuous few months in Washington with Democratic infighting threatening the Biden domestic agenda, including the two major infrastructure and social spending bills. Not only has the price tag of the Build Back Better Act (“BBBA”) been significantly reduced, so have the means of paying for the social package. The $3.5 trillion bill passed by the House Ways and Means Committee on September 13th not only sought to raise the corporate tax rate from 21% to 26.5%, but it also proposed several other tax increases and restraints on high income and high wealth individuals:

- Increase in the top income tax bracket from 37% to 39.6%

- Increase in the top capital gain and qualified dividend income rate from 20% to 25%

- Decrease in the Federal Gift and Estate Tax Exemption from $11.7M to $6M

- Limiting the use of valuation discounts for non-business assets

- Limiting the use of Grantor Retained Annuity Trusts (GRATs)

- Estate inclusion for Grantor Trusts

Modified Tax Implications Are Now on the Table

Political resistance to many of these provisions subsequently changed the tone of the debate. To move along the stalled legislation, on October 28th the White House released a revised “Build Back Better” framework. The House quickly followed with text of the latest version of the legislation which seeks several sources of funding:

- 5% surtax on incomes greater than $10M (including capital gains and dividends)

- An additional 3% surtax on incomes greater than $25M

- 15% minimum corporate tax on corporations with more than $1B in profits

- 1% excise tax on corporate stock buybacks

Financial Planning Considerations

Despite many competing interests (along with an intertwining of the Senate passed infrastructure bill), a strong push to get the BBBA over the finish line is in motion as we write, yet final details are still not clear. No matter how this plays out, it is important to take a moment and consider reviewing your tax planning and estate plans heading into year-end.

- Are your documents updated to address any recent life events?

- Are your named fiduciaries (Trustee/Personal Representative) still appropriate?

- Are your assets properly titled in accordance with your estate plan?

- Are you taking advantage of gifting opportunities (including charitable giving)?

- Are you maximizing your retirement contributions?

- Are you taking advantage of Health Savings Account contributions?

- Are you considering the potential merits of a Roth conversion?

We are happy to discuss the potential tax impact of the pending legislation and will pass along final details as soon as they become available.

For questions concerning our financial planning or wealth management services, please contact

Jim O’Neil, Managing Director, 617-338-0700 x775, [email protected]