Insights & Observations

Economic, Public Policy, and Fed Developments

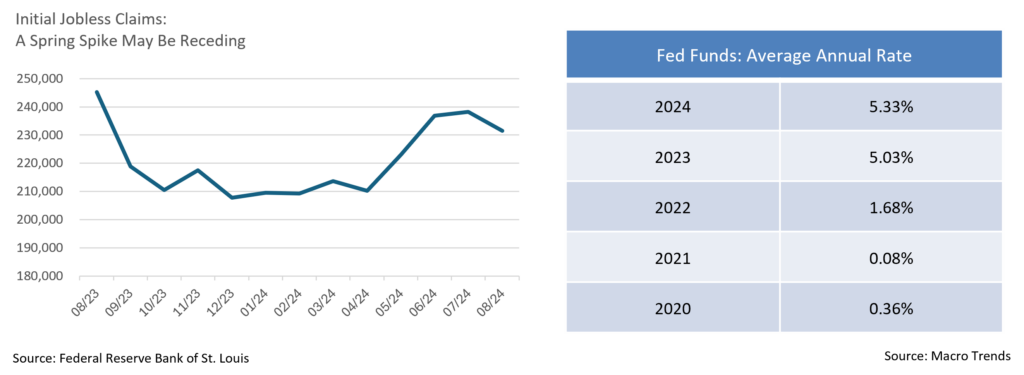

- Cyclical change is often clearer after the fact than during the process. Inflation has garnered the lion’s share of economic attention over recent years, the fight against which prompted 11 rate increases from 2022 to 2023 and a surge in Fed Funds from a record low 0.08% to today’s 5.33%, the highest level in over 20 years. For some time now, bad economic news has effectively been good news, as equities have tended to rally on the perception that progress in the fight against inflation would open the door to Fed rate cuts. That psychology may be changing.

- A turning point came on 8/1 and 8/2 with initial monthly jobless claims of 249,000 exceeding consensus estimates, ISM missing (46.8 vs. 48.8), and non-farm payrolls falling far short of expectations (+114,000 vs. +175,000), all of which set off alarm bells. A macro backdrop intensely focused on when the Fed would be at liberty to start reducing rates quickly turned to recession risk and whether monetary policy was behind the curve with cuts needed quickly. Over two trading days, the S&P 500 fell -3.20%, and 10Yr UST yields declined by 24bps. A rapid unwinding of the Yen carry trade involving borrowing ultra-low-interest rate currencies and reinvesting in a higher yielding US$ only exacerbated early August’s volatility.

- With a turn in monetary policy almost certainly upon us, market participants have become far more focused on the magnitude of rate cuts than their timing. Chairman Powell’s comments at the Jackson Hole Conference all but assured that September’s FOMC meeting will deliver a much-anticipated cut. Headlines eagerly reported Powell’s statement that “the time has come for policy to adjust,” and 2Yr UST yields quickly fell 12bps from 4.01% at the 8/22 close to 3.89% at the end of 8/28 trading.

- What curiously drew less attention was “the balance of risks,” a data dependent Fed assessment of economic conditions and policy response. The post-pandemic surge in global inflation has definitively moderated, and favorable comparisons to August and September 2023 (+0.6% and +0.4%, respectively) may soon result in annualized inflation reaching the Fed’s all-important 2% annual target. At this stage, we would argue that policy deliberations are focusing more on risks to growth and employment than inflation, as well as what the size of rate cuts will signal about the economy.

- The persistence of yield curve inversion is noteworthy, and with roughly a 150bps gap between Fed Funds and 2Yr USTs, this is the longest and widest inversion on record, a reality that suggests recession risk remains. Housing activity has slowed, and recent labor reports have been relatively weak, but not alarming. We are not currently in the recession camp and still see a “soft landing” as likely, although it may be a bumpy process. A series of recent reports suggests GDP growth is slowing back towards its long term +2% trendline, not recessionary levels, and late August data reported an in-line to slightly better than expected jobs report, as well as a reassuring PCE inflation print.

- Post-Labor Day ISM and labor market reports will be revealing and closely watched by the Fed. Today’s debate centers on the size of September’s pending cut, and we are of the view that the market will get 0.25%, not 0.50%. The latter would be politically problematic and holding off until November’s meeting allows the Fed to get past the election and assess two more months of economic data. CME Fed Watch is now calling for 100bps by year-end, an expectation that seems high to us unless the economy deteriorates more than we expect. Viewed through the prism of the equity markets and other risk assets, a “good news is good news” environment is back, as reassuring economic data will give the Fed license to ease in a slow and orderly manner, whereas large cuts risk signaling greater concern.

Equity News and Notes

A Look At The Markets

- Equities were mostly higher in August as the S&P 500 gained +2.3% to bring its YTD total return to +19.5%. The index had its best August in 3 years, is on a 4-month winning streak, and is up in 9 out of 10 months. Both the Nasdaq (+0.7%) and DJIA (+1.8%) trailed the S&P 500 but posted modest gains, while the Russell 2000 (-1.6%) gave back some of July’s outsized returns (+10.1%). Defensive and interest rate sensitive sectors outperformed, led by Staples (+5.8%) and Real Estate (+5.6%), while Energy lagged, falling -2.3% on a -5.6% drop in WTI crude oil.

- August got off to a rocky start as the S&P 500 dropped -6% in the first three trading days following a weaker than expected July jobs report. With the unemployment rate ticking higher to 4.3%, investors feared that the Fed was behind the curve and not moving quickly enough to cut rates. The Bank of Japan simultaneously raised their interest rate catalyzing a short covering of the yen and an unwind of the popular yen carry trade. These events culminated in a historic spike in the VIX, which touched 65 on 8/5 in what was the largest intraday jump on record. As astonishing as that move was, the subsequent collapse in volatility was equally impressive as the VIX fell from >50 to <15 on 8/15.

- A step up in corporate buybacks was a meaningful factor in the sharp rally off the early August lows. Goldman Sachs’ buyback desk saw volumes over 2x their daily average during the first week in August as companies looked to capitalize on the spike in volatility. Buyback authorizations also expanded with $107 billion of new announcements, the most ever in August. According to Goldman Sachs, these fresh authorizations should supply the market with $6.6 billion of daily purchasing power through 9/13 when the buyback window closes ahead of Q3 earnings season.

- The breadth expansion highlighted in our last report was sustained in August as technology leadership continued to wane. While the traditional market-cap weighted S&P 500 rallied to close the month within 1% of its all-time high, the equally- weighted S&P 500 finished 2.5% above its prior peak. The cumulative advance/decline line, an indicator of market breadth measuring net advancing stocks traded on the NYSE, also made a new all-time high in late August. We expect this to continue provided the market remains confident that the Fed can navigate an economic soft landing.

- One notable change to the market narrative came through a shift in focus from inflation to the broader economy, specifically the labor market. July’s CPI report came in as expected with the 3-month annualized core measure at +1.6%. Similarly, core PCE, the Fed’s preferred inflation measure, came in at +1.7%, well below the 2% Fed target. Chairman Powell pleased proponents of easing in his Jackson Hole speech saying “the time has come” to dial back monetary policy restriction and that upside risks to inflation have diminished. The market is now pricing in at least a single 0.25% cut at the 9/18 FOMC meeting, with ~30% odds of a 0.50% cut. Odds of a 0.50% cut will surely increase if the economy shows growing signs of teetering, but our base case remains 0.25% for the coming meeting. The August BLS report to be released on 9/6 will go a long way in settling the debate.

- As we move into September, it is hard to ignore the historic seasonal pattern of downside equity market volatility. Given the strength of equities to this point, it would be entirely reasonable to see a period of consolidation as the market works through a potential leadership change, geopolitical risks, a change in Fed policy, and the upcoming US election. We’ll continue to watch the economy and what bond yields are signaling but expect to be buyers of any significant dips. Our constructive outlook is backed by strong credit conditions, an easing Fed, positive corporate earnings growth, and improving breadth signals observed over the past months.

From the Trading Desk

Municipal Markets

- As we say goodbye to summer, we also say farewell to the very large reinvestment capital of the summer season. During these months, the municipal market enjoys significant support from the bond maturities and calls that investors are looking to put back to work. However, as we look forward to the fall and end of the year, the market will not have that crutch, and we may see some added volatility around seasonal issuance spikes.

- Supply has been at the forefront throughout the year and that dynamic continues. According to Bloomberg, August bond sales were about $50 billion, the biggest month year-to-date, evoking similar sentiment as previous election year spikes. The trend of increased issuance ahead of elections is largely due to issuers aiming to avoid potential volatility surrounding the presidential election. So far this year, issuance has consistently run ahead of last year’s numbers and is currently up about 35%.

- We expect that the combination of increased supply and limited reinvestment demand could elevate yields, providing an opportunity for municipal buyers. The 10-year AAA Muni/Treasury ratio is hovering around 70%, and if supply remains elevated this could push ratios higher, adding potential value for municipal investors.

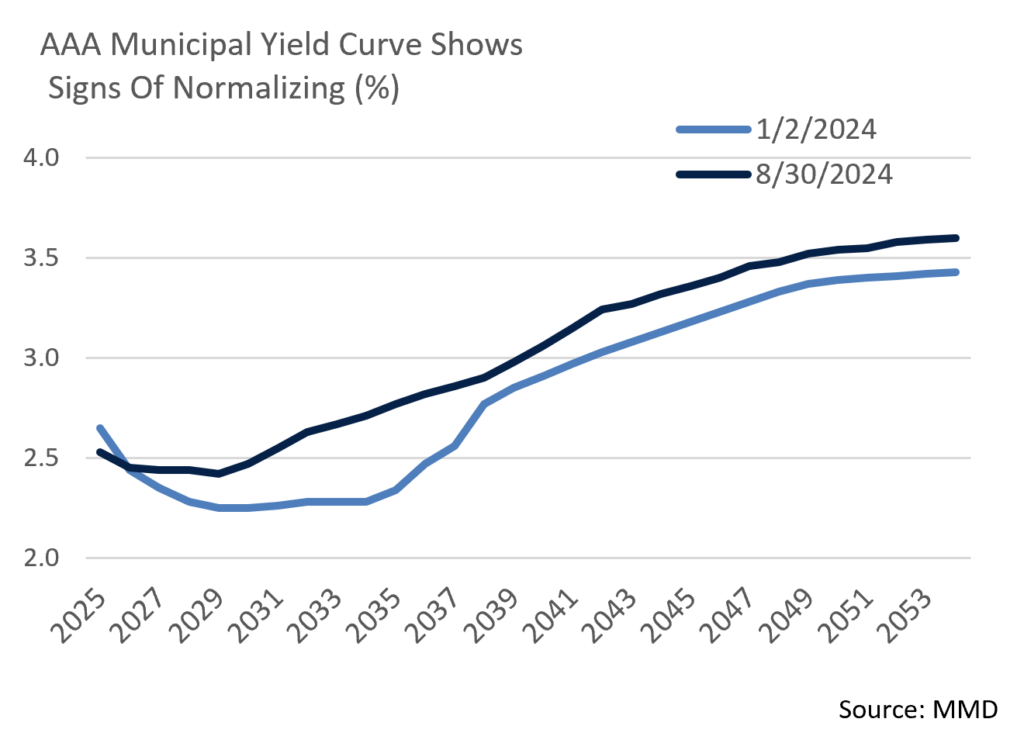

- The municipal curve has been working towards normalization for some months now and signs suggest that we are approaching a typical, upward sloping yield curve. Despite portions of the curve remaining inverted, the spread between 2Yr and 10Yr AAAs is +26bps, the highest we have seen during this normalization process.

- As the structure of the yield curve evolves, we are adjusting our Intermediate strategy buying pattern accordingly. When the curve was significantly inverted, we were finding the most value on the tails of our buying pattern: 1-3 years and 9-12 years with limited exposure in the trough of the curve, creating a barbell shape. We are now actively looking to add exposure in the belly of the curve as yields of those maturities increase. This will bring our maturity exposure closer to a bell-shaped distribution as a means of better capturing the value of an upward sloping yield curve.

Corporate Markets

- The backdrop for Investment Grade credit issuance remains favorable and issuers have been taking advantage throughout the year. However, August was slower than anticipated with only $108.6 billion coming to market vs. the $125 billion expected by syndicate desks. This was not terribly surprising, as August is a seasonally slower issuance month, although the total fell far short of $161 billion issued in the same month of 2023.

- This does not feel to us like the start of a slowdown trend, and it could be a useful break before an expected onslaught of deals in September. For months, issuers have been preparing for a widely expected Fed Funds Rate cut in September followed by the US election. Both could create market volatility, which tends to dampen issuance.

- At first glance, Investment Grade credit spreads seemed calm as August ended at the same OAS level as it began, although viewed more closely, the month brought heightened spread volatility. The month began with a spike in OAS on the Bloomberg US Corporate Index from 83bps to 111bps just 4 trading days later. That was the highest spreads have hit all year and a level not seen since November 2023. This quick risk-off adjustment was prompted by a lackluster jobs report on 8/2. As with equities, this was later seen as an overreaction as buyers soon returned in earnest, driving OAS back to 93bps later in the month. Until the Fed takes action to reduce the Fed Funds rate and offer insight into forward monetary policy, the markets will likely remain highly reactive to economic data and other market news, although we continue to anticipate a range-bound market.

- Through the end of July, $16,687 billion of new gross US Treasury supply has been sold. That is up 43.2% YoY and has facilitated a net cash raise of $950 billion. Peak issuance came in 2020, a period marked by massive pandemic relief, as $20,951 billion was sold with net cash raised of $4,282 billion. This year’s issuance surge has been led by demand for US Treasury Bills (1 year or less in maturity), although we expect to see greater demand for longer US Treasury Notes going forward given an expectation of falling short rates. More broadly, with $27.4 trillion of outstanding US Treasury debt, the market’s willingness to fund prolific federal borrowing without driving up yields remains a strategic risk. For now, demand has remained intact.

Financial Planning Perspectives

Charitable Gift Annuities – Are They Right for You?

There are numerous estate planning and charitable giving options available to individuals and their families, ranging from simple cash donations to sophisticated charitable trusts. With the passage of the SECURE Act and SECURE Act 2.0, charitable gift annuities have become an increasingly popular charitable planning technique because of the benefits they offer Donors and the charities they wish to support.

What is a Charitable Gift Annuity (CGA)?

Simply put, a charitable gift annuity (CGA) is a contract between an individual (or two individuals in the case of a joint and survivor annuity) and a 501(c)(3) nonprofit organization whereby the individual (Donor) makes a gift to the charity in exchange for a lifetime annuity payment. The annual amount of the annuity payment is based upon both the value of the gift and the Donor’s life expectancy (or Donors in the case of a joint annuity). Annuity payments, typically made on a monthly or quarterly basis, continue to be made for the life of the Donor or Donors.

What are the Benefits of a Charitable Gift Annuity?

In addition to receiving lifetime fixed annuity payments (some of which may be taxed federally or by states), the Donor also receives a partial income tax deduction for the year in which charitable gifts were made. For those who itemize, income tax deductions are based upon two factors:

1.The amount of the charitable gift; and

2.The age of the Donor (or Donors in the case of joint and survivor annuity).

Along with supporting the purpose and mission of the charity, a valuable opportunity afforded Donors through CGAs lies in the ability to fund the annuity with highly appreciated stock. In this scenario, a Donor may be holding low basis stock that would incur a substantial capital gains tax if sold. Donating through a CGA structure allows one to avoid having to pay capital gain on stock appreciation while also generating a stream of income.

In furtherance of funding a charitable gift annuity with cash or securities, the SECURE Act 2.0, passed in December 2022, allows individuals 70 1/2 years or older to make a one-time Qualified Charitable Distribution (QCD) from an IRA to a CGA. The current limit to this one-time QCD to a CGA is $53,000, a cap that is indexed for inflation. While funding the charitable gift annuity in this manner does not provide an income tax deduction, it counts toward satisfying annual required minimum distributions (RMDs), and the transfer to the CGA will not be included in income for tax purposes.

How Do Charitable Organizations Set Charitable Annuity Gift Rates?

Most large charitable organizations belong to the American Council on Gift Annuities (ACGA). The ACGA was established in 1927 as the Committee on Gift Annuities and was created to assist nonprofits in determining prudent rates of interest to be paid on charitable gift annuities. ACGA publishes suggested maximum rates on an annual basis for both single life charitable gift annuities and joint and survivor charitable gift annuities (www.acga-web.org/current-gift-annuity-rates).

Is a Charitable Gift Annuity Right for Me?

Optimizing charitable giving differs on a case-by-case basis along with client assets, goals, family circumstances, and tax circumstances. Regardless of the technique or charitable vehicle employed, a constant lies in the desire to efficiently support charitable organizations whose purposes align with your philanthropic objectives. If you have questions or would like to further explore charitable giving options, please reach out to your Portfolio Manager or Jim O’Neil.

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.