Insights and Observations

Economic, Public Policy, and Fed Developments

- After an escalation in US rhetoric before the G20 summit in Buenos Aires, President Trump and President Xi agreed to a “truce” in the trade war. Details are sparse, and the tone of Chinese media interpretation differs from US reports, but it appears both sides have agreed to a 90-day hiatus on additional tariffs, including previously-announced increases set for January 1st. Domestic equity markets gave up all of their gains and more after initially surging on the news, as the market struggles to digest an agreement to essentially continue talking.

- President Trump also told reporters he would begin the process of officially terminating NAFTA on the return flight from the G20 summit, a stance taken to increase pressure on Congress to approve his USMCA replacement deal. We view this as a modest negative, as the USMCA was likely to pass in some form. This move effectively seems to raise the consequences of a misstep.

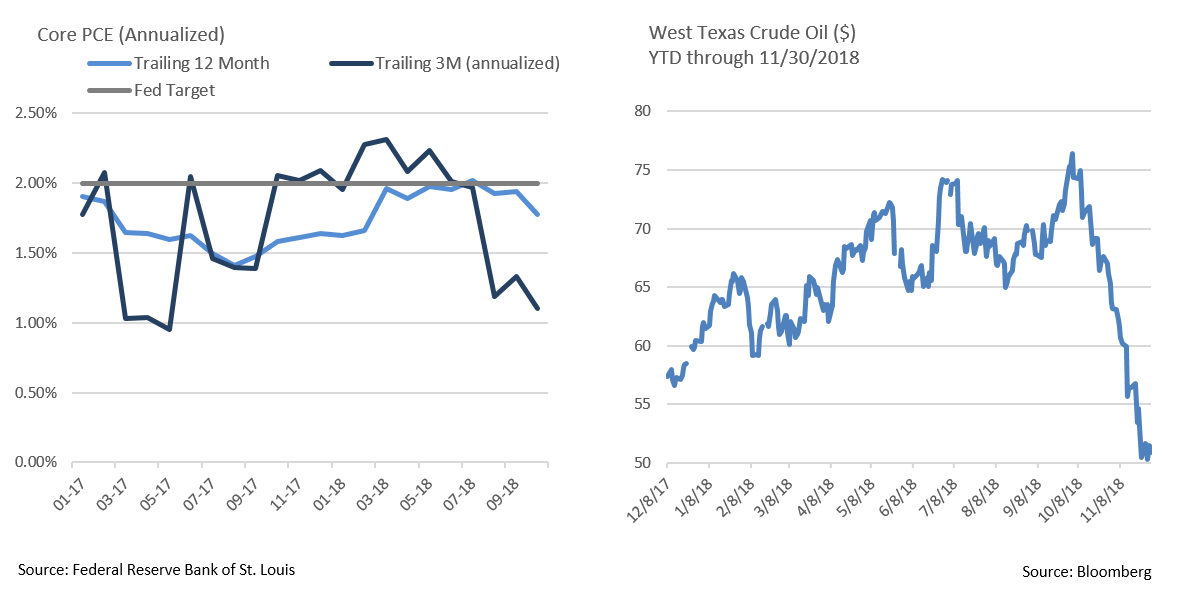

- As we had projected, the Fed’s preferred inflation measure, core PCE, fell on a YoY basis in October. Between a weak 0.1% October reading and a downward revision in September, core PCE fell from 2.0% to 1.8%. Headline missed as well, remaining at 2.0% vs expectations of 2.1%. Trailing 3-month core PCE now stands at an annualized 1.1%, well below the Fed’s 2% policy objective. Continued weakness in inflation data may make it difficult for the Fed to continue its current pace of rate hikes. Indeed, the Fed Funds futures market now does not consider a 2019 rate hike more likely than a coin flip until June, and the probability of two or more hikes occurring by the end of 2019 is only about 1-in-3. However, escalating political pressure from the President to not “hike” complicates the analysis.

- Q3 GDP came in unchanged at 3.5% in the first revision. Business investment, a large driver of growth in the first half, was revised up from 0.8% to 2.5%, while household spending weakened slightly from 4% to 3.6%. Nothing in the revision changes our outlook for a slight deceleration in the economy’s growth rate in the last quarter of the year.

- Oil entered correction territory in November, dropping from October’s intraday high of $76.72 to close the month at $50.93. Slack demand coupled with booming supply, particularly in US shale oil production, pulled prices lower. Low oil prices are a boon to consumers in the short run, but could have a dampening effect on the US economy (where the oil patch is a significant employer) and continue to weigh on inflation.

From the Trading Desk

Municipal Markets

- The latter half of November saw the municipal market strengthen with yields on the 5 to 10-yr portion of the AAA curve declining by 10–15 basis points. Weak housing numbers, reduced inflationary expectations, and concerns about slowing global growth prompted Treasury demand, and high quality munis generally followed suit.

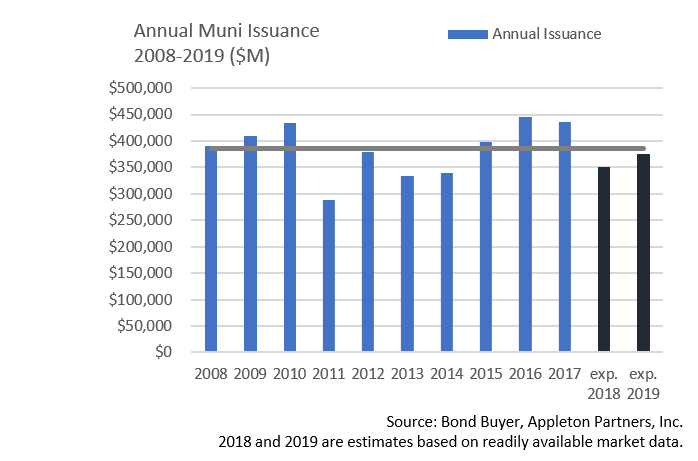

- The muni market has been supported in 2018 by tight supply. YoY issuance will end down significantly, in part due to issuers accelerating deals at the end of 2017 ahead of 2018 tax changes. As we look to 2019, strategists are expecting $375 – $380 billion in supply, an estimated 6-7% increase vs. the current year. Low Q1 2018 supply creates easier forward comparisons, and an expected increase in infrastructure project financing should also facilitate a growth in 2019 supply. Even assuming these estimates prove accurate, 2019 would still see net negative issuance, a positive technical factor.

- With nominal yields rising, the 10-Yr AAA muni ended November at 2.51% vs. 1.98% at the beginning of 2018. With increased 2019 issuance likely, we anticipate good opportunities to put assets to work.

- We also see an environment conducive to moving up in credit quality. Tight credit spreads have reduced the muni risk premium of lower-rated bonds. With the market offering relatively low compensation for taking credit risk, portfolio reallocations that enhance credit quality merit consideration.

Taxable Markets

- Corporate and Treasury sentiment in November followed a very similar path as the prior month, beginning on positive footing, but ending with risk assets out of favor. IG credit spreads pushed through 2-year highs to end the month, with the Bloomberg Barclays IG Index widening by 22 basis points to 137 over Treasuries. Uncertainty regarding global economic conditions was the primary culprit.

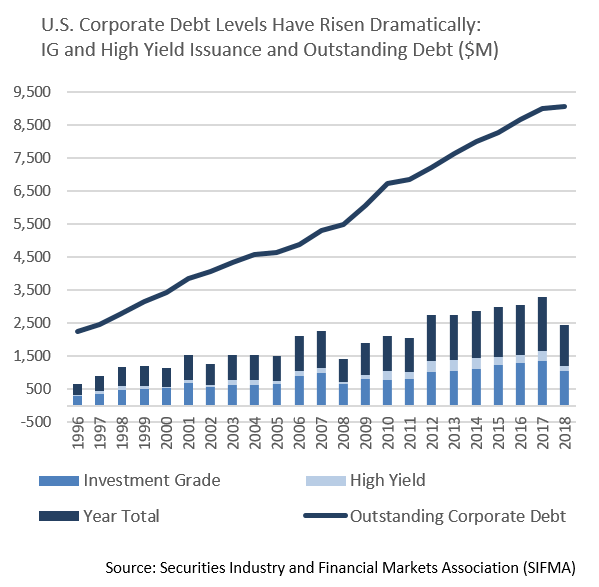

- Outstanding High Yield and lower quality IG debt has climbed to record levels, a development that has the Fed’s attention. The November 2018 FOMC meeting minutes stated that “several participants were concerned that the high level of debt in the non-financial business sector, and especially the high level of leveraged loans, made the economy more vulnerable to a sharp pullback in credit availability, which could exacerbate the effects of a negative shock on economic activity.” Lower grade credits tend to be more vulnerable to deteriorating market conditions, as once again demonstrated by reaction to recent equity volatility and slumping oil prices. While we do not anticipate an impending credit event, our higher quality orientation should help insulate portfolios as the market grapples with Fed policy and the economic outlook.

Public Sector Watch

Mid-Term Election

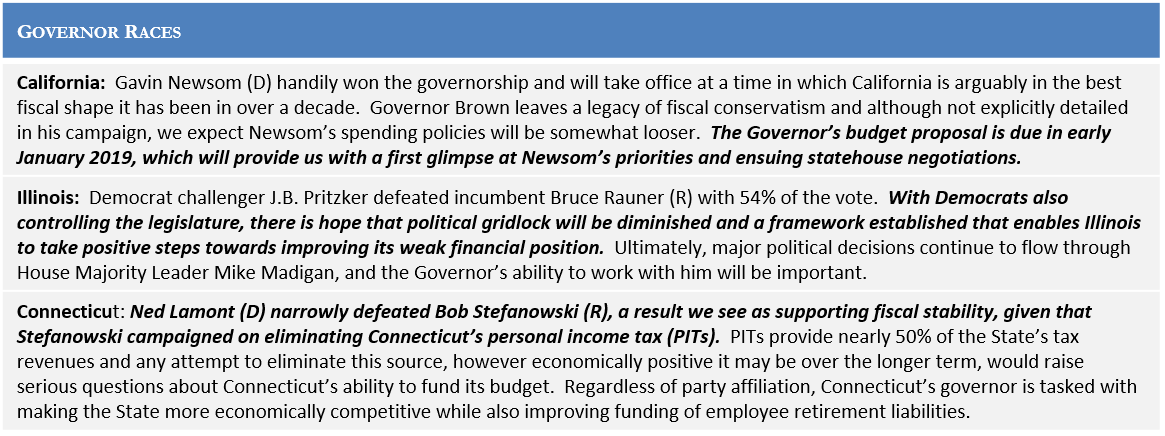

Although the lion’s share of attention during the 2018 mid-term elections was paid to the battle for Congress, numerous ballot measures, bond authorizations and governorships were also decided by voters last month. We reference a few with particularly meaningful credit implications.

Ballot Measures

California – Proposition 5: Failed

- Proposed allowing homeowners aged 55 or older to transfer their lower tax assessment to a new home. We see defeat as a positive outcome for local governments as it would have resulted in lower property tax inflows.

Connecticut – Amendment 1: Approved

- Passage creates a constitutional protection for transportation revenues which will now only be available to fund transportation infrastructure, not general government operations. We view this as modestly positive for Connecticut special purpose bonds and the State’s overall credit profile, although the amendment’s somewhat vague wording raises Connecticut-specific questions that give us caution.

Bond Authorizations

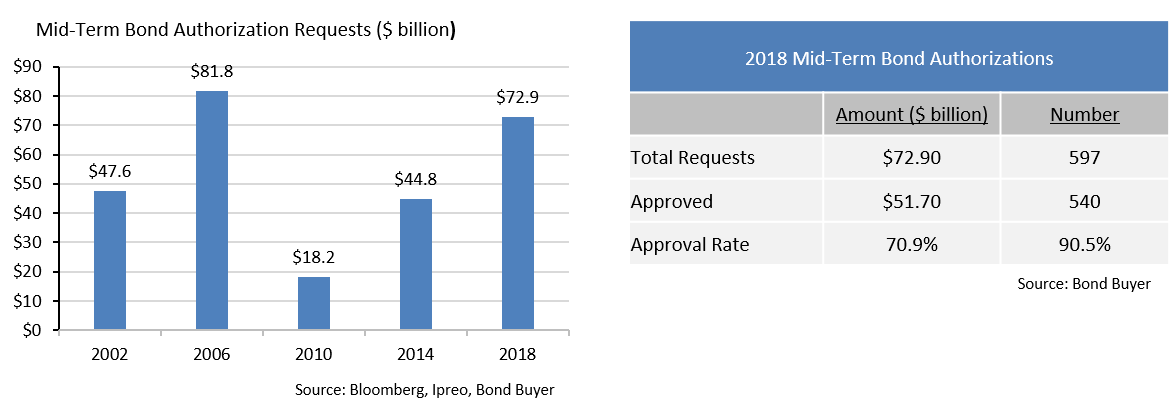

- State and local governments placed $72.9 billion of bond authorization requests on the November 6th ballot, well above the average of $48.1 billion over the last four mid-term elections. This year saw 71% of authorization value approved, down from an average of nearly 79% since 2000. We do not see this as reflecting voter unwillingness to entertain new bond authorizations, as the approval rate measured by number of requests reached 90%. Despite the defeat of a handful of large bond measures, most notably CA – Water Projects ($8.9 billion); CO – Transportation Projects ($6.0 billion); and CO – Road and Bridges ($3.5bn), the data suggests that voter support for essential government infrastructure and services remains strong.

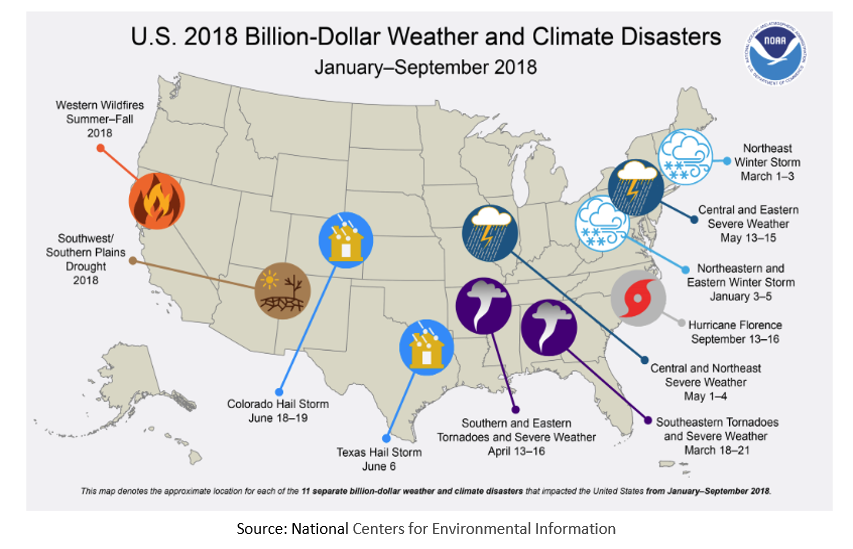

California Wildfire Impact

- The recent California wildfires have caused unprecedented, catastrophic loss of life and property. The Camp Fire north of Sacramento has been deemed the deadliest and most destructive on record. While now fully contained, many areas remain under evacuation orders, making it difficult to fully assess the magnitude of damage. While the humanitarian impact is paramount, as investors we must also look at credit implications.

- In the aftermath of natural and other disasters, the value of municipal bonds has historically remained unimpaired. Debt service payments have continued, as efficient access to the capital markets is critical. While immediate increased costs for emergency personnel, housing of displaced residents, and clean‐up demands are significant, many local governments have liquidity reserves they can tap to support these efforts. Local governments already experiencing financial stress have been disproportionately negatively affected, as disasters exacerbate existing budget challenges. We expect that those entities with sufficient resources, solid management, and access to capital will be able to maintain credit quality as the CA clean‐up and rebuilding process unfolds.

- The State and the Federal Government have declared California a disaster area, expediting emergency personnel and financial assistance to affected areas. FEMA public assistance will cover over 75% of the costs related to publicly owned facilities, with state disaster relief helping to close the remaining gap. We also note that unlike flood insurance, residential fire insurance coverage exceeds 90% nationally and is much more commonly held by homeowners. Insurance proceeds, federal aid, state financial support, and private contributions have ultimately provided a boost to economic activity over the long-run in impacted regions, due to the impact of economic stimulus.

- What is different this time is that the Camp Fire had a devasting impact on one community, the Town of Paradise. This is a tragedy with potential precedent setting implications. Past fires have generally destroyed small percentages of a local tax base and ultimately had muted effects on overall credit quality. The destruction of a town of 27,000 residents is unprecedented. Damaged infrastructure, economic disruption, and the possibility that a majority of the population will not return has the potential to drastically compromise its tax base. At year-end 2017, the Town had $37.5 million in notes, bonds, capital leases, other post-employment benefits (OPEB), CalPERS pension liability and compensated absences outstanding, raising questions about how these obligations will be serviced.

- Appleton Partners does not have direct exposure to the Town of Paradise. However, we are watching developments and the bond market’s reaction closely. With wildfire activity increasing in magnitude and frequency, how the Town of Paradise’s crisis plays out may become a test case for the future.

Strategy Overview

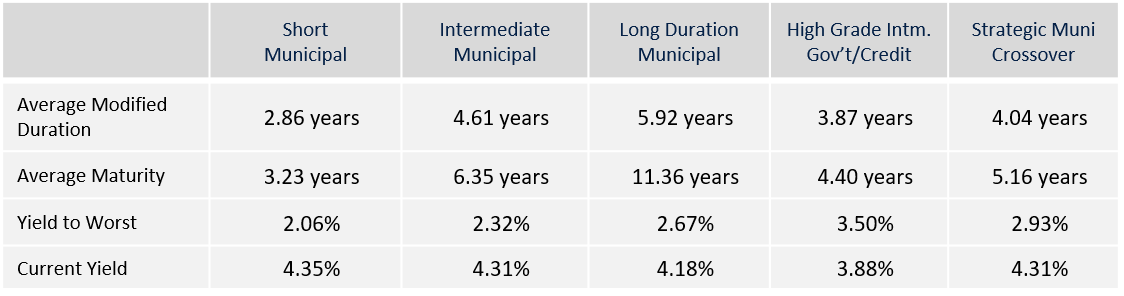

Portfolio Positioning as of 11/30/2018

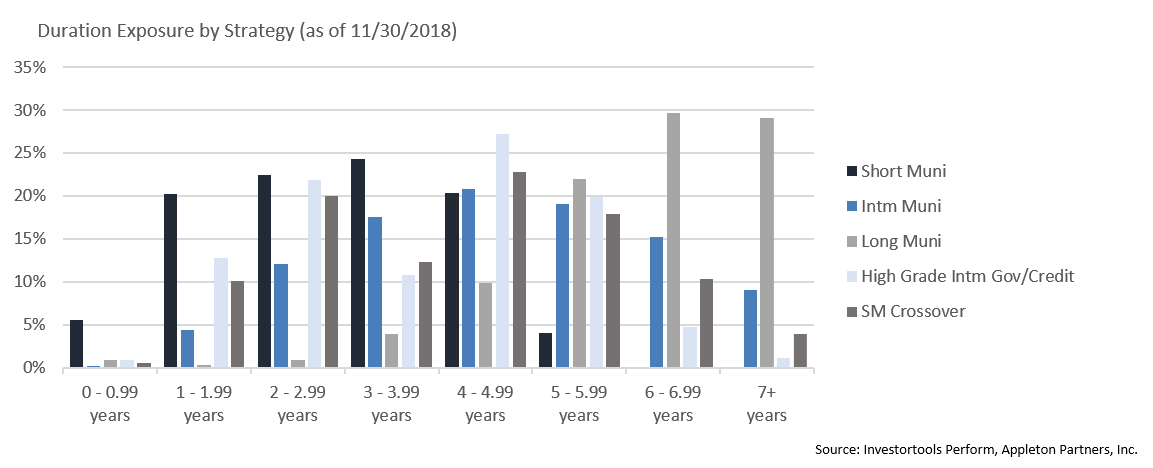

Duration Exposure by Strategy as of 11/30/2018

Our Philosophy and Process

- Our objective is to preserve and grow your clients’ capital in a tax efficient manner.

- Dynamic active management and an emphasis on liquidity affords us the flexibility to react to changes in the credit, interest rate and yield curve environments.

- Dissecting the yield curve to target maturity exposure can help us capture value and capitalize on market inefficiencies as rate cycles change.

- Customized separate accounts are structured to meet your clients’ evolving tax, liquidity, risk tolerance and other unique needs.

- Intense credit research is applied within the liquid, high investment grade universe.

- Extensive fundamental, technical and economic analysis is utilized in making investment decisions.