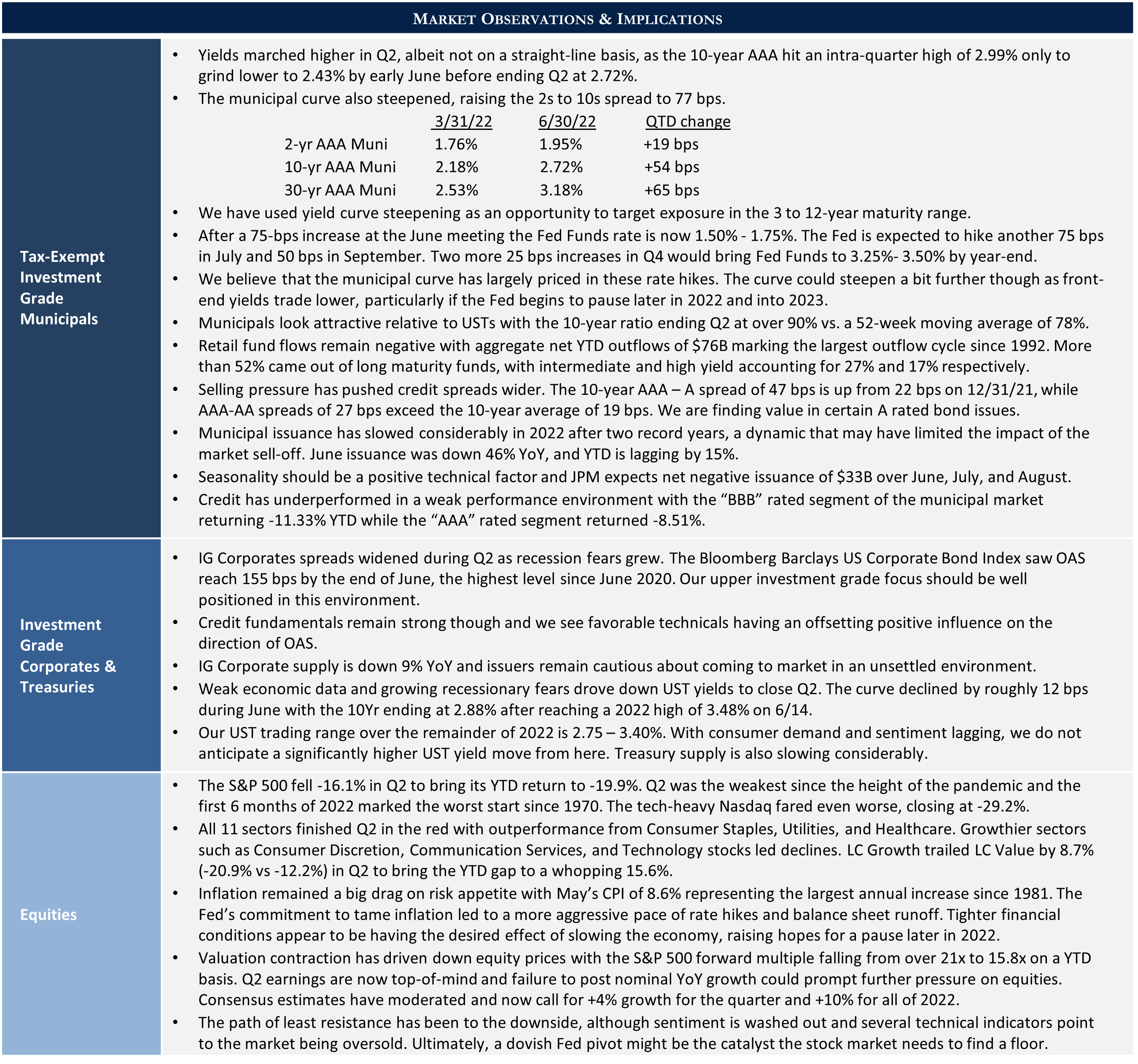

An Approaching Demographic Sea Change

Generation X households are likely to inherit a staggering $30 trillion in wealth over the next 25 years and overtake the Baby Boomers as America’s wealthiest generation.1 The magnitude of this dynamic has caught the attention of wealth management professionals, and what is unfolding in an aging America is also likely to have a profound effect on individual relationships with money.

Looking forward, we see a need for many of our clients to find a way to draw younger family members into their estate and overall financial planning process. Doing so can be integral to helping the next generations not only more successfully manage potential future inheritances, but also navigate their own financial lives in a society that has rapidly pushed responsibility onto the individual. These two challenges are quite different in certain respects but similar in terms of the need to understand financial concepts and ultimately make good decisions. How prepared are your children and grandchildren to tackle a lifetime of investment and related economic matters?

Ensuring Intergenerational Success

The importance of engaging family members in personal financial matters has been amplified by a profound change in the relationship between employment and retirement over recent decades. Our once paternalistic system of pension plans complemented by Social Security has clearly receded with only 15% of private-sector workers currently having access to a Defined Benefit plan.2 The demise of private sector pensions has placed a burden on individuals, many of whom are entering the work force or moving through their peak earning years without sufficient financial background or guidance.

As advisors, we often find that clients measure the ultimate success of their wealth management plans at least partially through the extent to which their legacy and family objectives are realized. Ensuring loved ones have adequate financial know how as they navigate their careers and personal lives is a key ingredient in successful multi-generational wealth management. What might facilitate future success in this regard and how can Appleton help?

It Starts with Financial Literacy

Establishing a baseline level of knowledge and experience can help your loved ones understand and carry out your wealth transfer and legacy wishes, while also bolstering their ability to make wise economic and investment decisions in other aspects of their lives. Whether it relates to establishing and adhering to a long-term asset allocation strategy, building retirement savings, funding education and other future liabilities, mortgage financing and debt management, constructive involvement with you and your portfolio team can be beneficial.

As a practical example of the challenges many face, consider that a 2022 TIAA Institute study revealed that US adults could only answer 50% of basic financial literacy questions correctly and a mere 36% relating to investment risk (defined by the uncertainty of investment outcomes).3 Furthermore, while education and income were found to be positively correlated with financial literacy, those earning $50,000-99,999 and greater than $100,000 annually fared only marginally better, answering 51% and 60% correctly.

Absent adequate financial knowledge, managing an inheritance, navigating turbulent market cycles such as we are currently experiencing, or simply taking the right steps to build long-term retirement savings can be more difficult. As a society, we have not prioritized financial literacy, yet resources are available, one option being through The National Endowment for Financial Education.

Take Proactive Action Steps

So, how does Appleton fit into the equation? Above all, we encourage clients to think about where they see planning and educational gaps within their families. No one approach works for everyone, although we suggest leveraging our resources to help subsequent generations become more conversant and comfortable with wealth management and your specific plans.

Our Private Client Services team prioritizes offering practical, easily digestible guidance concerning multi-generational planning issues. We recognize the magnitude of the challenge and are trying to help in part by providing information that can be easily shared with other family members. Our financial planning webinar series tackles topics such as “Financial Consequences of Adulthood,” “Equity Analysis Concepts,” and “Women and Financial Planning,” among others. We also emphasize short written briefs that cover matters such as social security distributions or college planning. Our goal is to raise awareness and share actionable advice. We encourage you and your family members to visit our website to access a variety of content of this nature.

Personal finance hardly needs to become one’s hobby. What matters is ensuring your loved ones possess a sufficient level of knowledge and understanding of the core concepts that will ultimately impact their ability to manage often complex financial lives, a process that may also one day involve an inheritance. Drawing family members into your planning process can be a good way to start. Your Appleton portfolio management team is here to help, and we encourage your input into what might work best for your family.

- Cerulli Associates

- March 2021 National Compensation Survey from the Bureau of Labor Statistics

- 2022 TIAA Institute-GFLEC Personal Finance Index (P-Fin Index) — an annual survey measuring US adults’ financial literacy levels across eight functional areas

This commentary reflects the opinions of Appleton Partners based on information that we believe to be reliable. It is intended for informational purposes only, and not to suggest any specific performance or results, nor should it be considered investment, financial, tax or other professional advice. It is not an offer or solicitation. Views regarding the economy, securities markets or other specialized areas, like all predictors of future events, cannot be guaranteed to be accurate and may result in economic loss to the investor. While the Adviser believes the outside data sources cited to be credible, it has not independently verified the correctness of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed are, were or will be profitable. Any securities identified were selected for illustrative purposes only, as a vehicle for demonstrating investment analysis and decision making. Investment process, strategies, philosophies, allocations, performance composition, target characteristics and other parameters are current as of the date indicated and are subject to change without prior notice. Registration with the SEC should not be construed as an endorsement or an indicator of investment skill acumen or experience. Investments in securities are not insured, protected or guaranteed and may result in loss of income and/or principal.