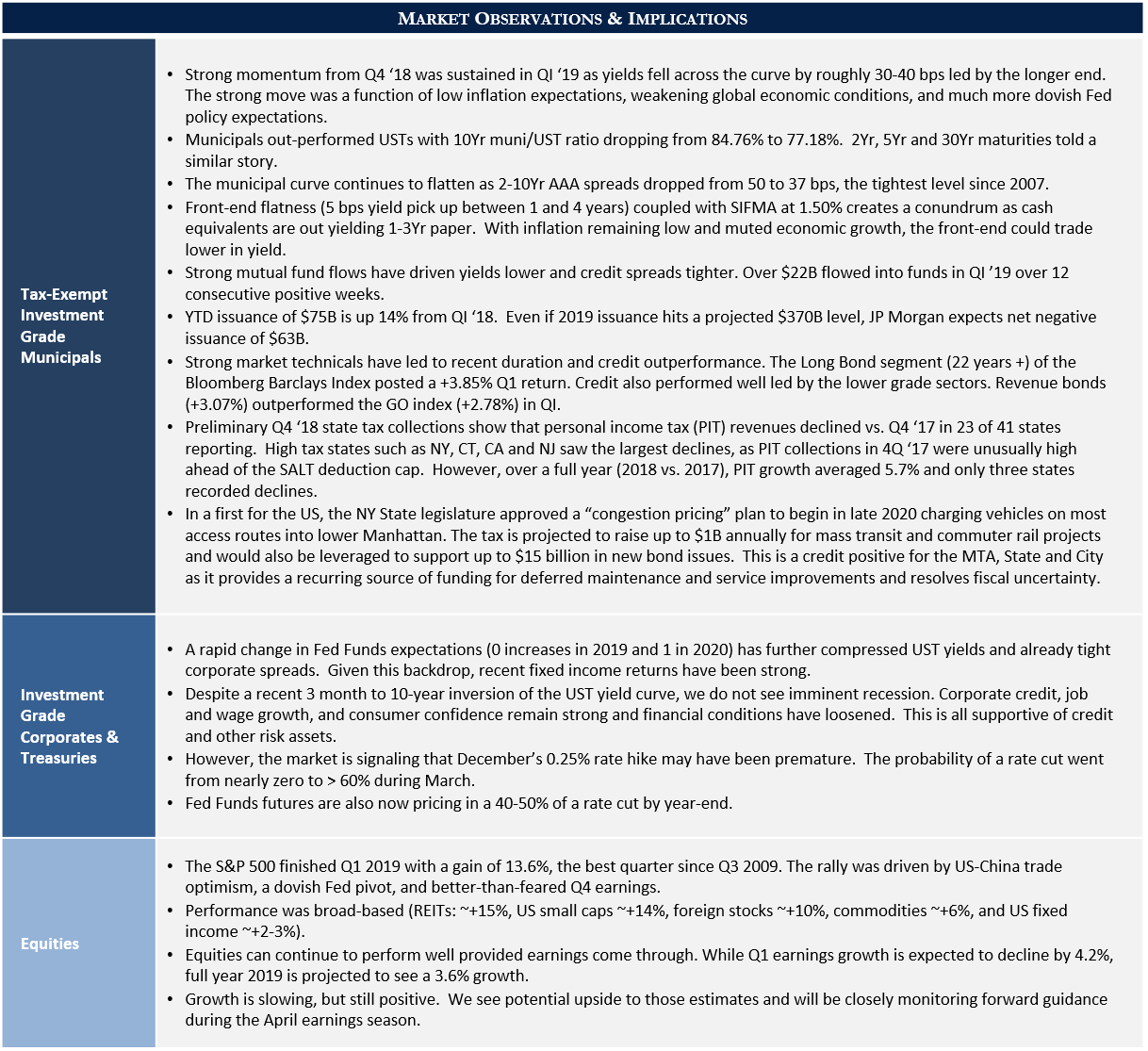

“The US economy is showing vulnerability to geopolitical risk, but – as Mick Jagger once sang in ‘Sympathy for the Devil’ – “as heads is tails,” a bear reading and a bull reading of the economy may explain the seeming contradiction of the first quarter. The two readings are at the end of the day still two sides of the same coin.”

The contradiction between the stock and bond markets in the first quarter couldn’t have been more striking. Equities were off to the races, with the S&P 500 posting its best quarterly return since Q3 2009. Meanwhile, the bond market was flashing warning signs of recession, with the 3-month to 10Yr curve inverting after the 10Yr fell like a rolling stone by nearly 30bps, coupled with Fed Funds futures abruptly pricing in about a two-in-three likelihood of rate cuts before year-end.

A sensible market observer would not expect to see these things happening simultaneously, yet here we are. While this scenario was beneficial to investors, with nearly all risk assets putting up unusually high returns, it’s also one that should give pause. Is the stock market right about the economy, or the bond market? Our answer is “neither.”

Moments of Doubt and Pain

There’s an old economist’s joke that an inverted yield curve has correctly predicted eight of the last six recessions. There’s a grain of truth behind that quip. The Treasury yield curve is normally upwards-sloping, meaning the longer an investor is willing to lock up capital, the higher yields they will earn. This compensates longer-term investors for the possibility that shorter, risk-free rates are higher at some point than they are today. When the curve inverts and becomes downward-sloping, it suggests investors either expect risk-free rates to fall, or are so eager to safely tie up money for longer periods of time that they’re willing to give up yield to do so. Both cases suggest uneasiness about the economy.

And there are plenty of reasons to feel that way. What seemed like a shutdown-related blip in retail sales in December has instead extended through February, and inventory levels have risen. Most measures of inflation have also ticked downwards, implying weak demand. Capital goods orders are stagnant, GDP growth weakened in Q4 and is expected to come in weaker still in Q1, and corporate earnings appear on track to decline for the first time since 2016. Fed Funds futures on 3/31 projected a 64% chance of a rate cut before year-end, reversing expectations from a mere six months ago. Complicating matters, President Trump has escalated his war on the Fed’s independence. From this perspective, it’s hard to discount reversion to the mean as an explanation for the S&P 500’s stellar first quarter.

All the Sinners, Saints

However, there’s a highly credible bull case here, too. Corporate earnings may be expected to drop in Q1, but investors typically focus on the second half when earnings growth is projected to resume. GDP may be decelerating, but this was expected after the stimulus effects of the Tax Cuts and Jobs Act wore off, and we appear to be settling back towards a post-Financial Crisis 2% real GDP growth trendline. Business confidence indices may have weakened, but only to roughly five-year average levels, hardly cause for concern. Forward price-to-earnings ratios may be a little stretched, but they are not significantly above recent averages. Even if feared yield curve inversions have been reasonably good – if imperfect – past recession indicators, 12-18 months of solid equity performance usually follows. And while the Fed notes the Fed Funds rate is below their long-term neutral rate estimate, they’ve also emphasized that it is at a short-term neutral level and that a pause is appropriate.

The Fed’s pragmatism is an encouraging sign – most past inversions occurred when the Fed pushed short rates too far, choking growth. In 2006, the curve inverted shortly after a rate hike and remained there for most of the year. The current inversion followed nearly three months of relative stability, lasted mere days, and occurred not because the short end increased, but after the long end fell on a contraction in German manufacturing. The cause of the yield curve’s inversion appears very different this time around, an overlooked factor that we believe has meaning.

Please Allow Me to Introduce Myself

Our view is that this inversion primarily reflects uncertainty due to geopolitical risk factors having little to do with the current health of the US economy. The US is engaged in extended trade negotiations with China, and while we continue to believe a modest deal is reasonably likely, there is still little clarity as to what that might look like. Further, the Trump Administration is also threatening tariffs on auto imports, which if imposed, would have negative economic ramifications at home and abroad. And finally, the clock is ticking on a wildly unpredictable Brexit saga with the end game yet to present itself. How these issues ultimately play out will have major implications for trade and overall global economic conditions.

Last month’s inversion in the curve looks more to us like a rational response to event risk than market conviction a recession is imminent. That’s not to say one is impossible. Investor risk appetites matter, “this time it’s different” stories are routine before recessions, and an external shock in a skittish market could lead to recession. Nonetheless, we believe that successful resolution of these largely geopolitical concerns would cause the stock and bond markets to re-focus on fundamentals and be valued in accordance with an economy experiencing 2% annual growth, low unemployment, and low inflation.

But What’s Puzzling You

So, we think neither the stock nor bond market has it right. The economy is unquestionably slowing. Equity markets are too sanguine about trade outcomes and future earnings growth, and we would welcome a period of consolidation to allow P/E ratios to tighten a little. Despite what today’s Fed futures are saying, we don’t see current economic conditions leading the Fed to start cutting rates and do not believe a recession is imminent. Rather, the US economy is showing vulnerability to geopolitical risk, but – as Mick Jagger once sang in ‘Sympathy for the Devil’ – “as heads is tails,” a bear reading and a bull reading of the economy may explain the seeming contradiction of the first quarter. The two readings are at the end of the day still two sides of the same coin.