Insights and Observations

Economic, Public Policy, and Fed Developments

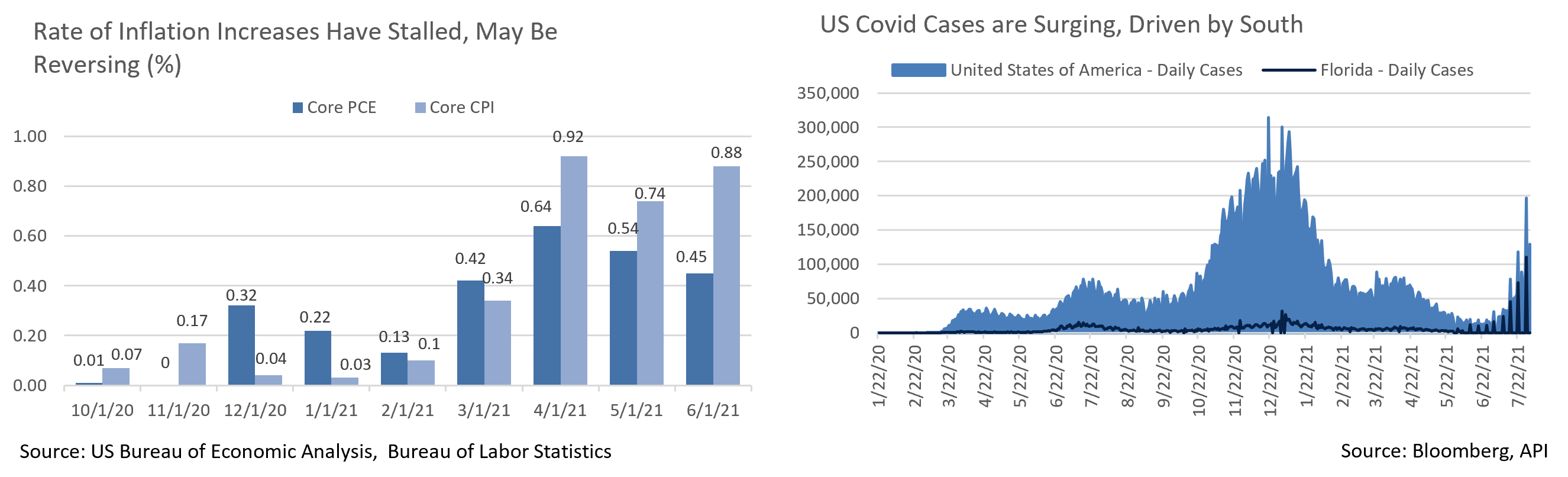

- The inflation narrative was the dominant market driver over the first half of 2021, and as we enter August, data appears to support the Fed’s belief that inflation will be transitory. Despite the market’s focus on upside surprises, the rate of increase in monthly readings has stalled out and, particularly the Fed’s preferred Core PCE, may be forming a downtrend. While it will be some time before year-over-year readings begin to recede due to earlier near-zero readings dropping out, inflation appears to have peaked.

- Additional support for a waning of inflationary pressure came from this week’s Manufacturing PMI Survey. While the headline number was encouraging and suggested moderation to a still strong but more sustainable level, the prices paid and delivery time sub-indices showed signs of moderating inflation. While these are still extremely high levels by historical norms, the data suggests that manufacturers are seeing pricing pressures ease and delivery times fall on manufacturing inputs.

- Durable Goods orders and retail spending also showed signs of moderation. June’s Durable Goods orders came in under consensus, +0.8% vs +2.2%. While prior period upward revisions partially offset the miss, the absolute level of orders were still low and most of the strength was concentrated in transportation equipment, which should help with backlogs. Ex-transportation, orders have now fallen for three straight months. Meanwhile, while retail sales beat, +0.6% vs -0.3%, prior period downwards revisions coupled with a +0.9% price increase component suggest purchasing is starting to slow off high levels. Michigan Consumer Sentiment sub-indices also offer evidence that consumers are starting to pull back on big-ticket purchases, with notable declines in the Large Household Vehicles, Homes, and Vehicle categories.

- Despite some initial resistance, the “Infrastructure Investment and Jobs Act” moved out of Senate committee comfortably, with 17 Republicans joining Democrats in a 67-32 vote to open debate, a sign that it may have enough support to pass. The bipartisan bill is now expected to total $1.2 trillion, including $550 billion in new spending over five years. The House still intends to pass the bill in lockstep with a larger “human infrastructure” bill that leaves Speaker Pelosi with a very narrow pathway to hold her slight majority caucus together. It remains unclear if the House “human infrastructure” bill has the votes to pass the Senate, even via budget reconciliation.

- Q2 GDP came in below expectations, +6.5% vs. consensus forecast of +8.4%. Below the surface, growth looked a bit stronger. A drawdown in inventories was responsible for a 1.1% detraction in headline GDP, as well-publicized supply chain issues weighed on growth. GDP would have still missed even if supply chains had been able to keep pace with demand, though by a lot less. As inventories are replenished some of Q2’s expected GDP growth will likely move into Q3.

- The Fed’s July meeting came and went with little event. The meeting was most notable in that it represented another opportunity for the Fed to adjust messaging and move up their taper timeline, although they instead held course. The most interesting news came out of the press conference, where Chairman Powell indicated there was “little support” at the Fed for tapering MBS purchases before Treasuries despite speculation they might move there first to cool a hot housing market.

- Unfortunately, the Covid-19 pandemic has been anything but uneventful recently, as cases have been surging, particularly in the South where vaccination rates are much lower. Although Florida’s “reopen at all costs” approach initially seemed to spare the state the worst of feared outcomes, cases began rising rapidly during July. The final week had Florida, a state with 6.5% of the country’s population, responsible for 25% of the nation’s new cases. Louisiana, South Carolina, and Mississippi show similar trends, though from lower bases. A return of widespread economic shutdowns still seems unlikely, although we are concerned about the human and economic costs a growing Covid wave could bring.

From the Trading Desk

Municipal Markets

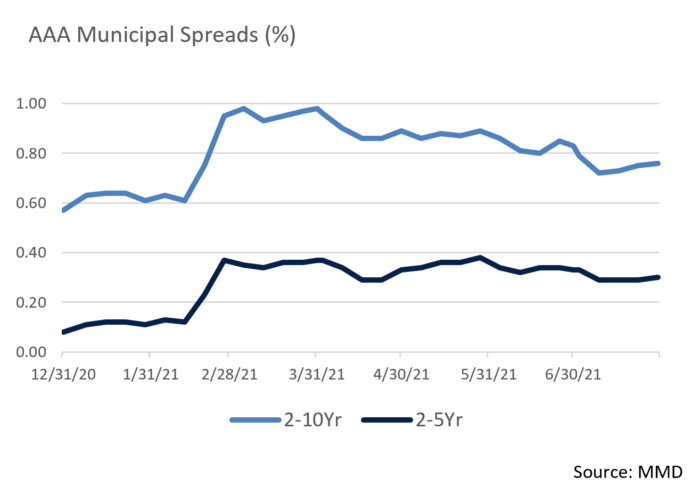

- The MMD curve flattened over the month with the 2-10Yr AAA spread declining from 83 bps to 76 bps, yet it remains significantly steeper than where we stood at year-end 2020 (57 bps). We continue to find value in the 5 to 9-year portion of the curve.

- During the month of July, taxable municipal issuance as a percentage of total issuance increased, suggesting there is still a desire for taxable advanced refundings. Year-to-date, taxable municipals as a percentage of the total is about 25%. Should US Treasury rates remain low, we expect to see continued issuance in that area of the market, leading to buying opportunities for those looking for taxable income.

- Peter DeGroot of JP Morgan recently looked at couponing in bonds over the first half of the year and noted that secondary trading of 5% coupons declined from 60% to 49% since the Tax Cuts and Jobs Act was enacted. The proportion of 4s and 3s increased marginally, although 2% coupons increased the most, rising from 3.6% in the first half of 2018 to 13.1%. We surmise that low yield levels and relatively higher dollar prices will cause this trend to persist. Couponing is an important element of bond structure, and we evaluate various structures in both the primary and secondary market to uncover value.

- Despite modest yields the song remains the same in terms of retail demand for municipals. Net municipal mutual fund flows reached $69.5 billion on a YTD basis as August began, with long-term funds garnering $42.45 billion. Broad credit strength, ongoing policy support, and potential high-income tax increases have all fueled a sustained desire for tax-advantaged income.

Corporate Bond Markets

- Investment Grade credit spreads continue to march along the path of least resistance as market technical factors and credit fundamentals remain positive. High grade spread volatility remains muted, although the OAS on the Bloomberg Barclays Corporate Bond Index bounced off a YTD low of 80 bps at the end of June to close the month at a still tight 87 bps. That is just 11 bps wider than where we began 2021. The modest tick up in credit spreads in March driven by inflation fears has since abated due largely to a dampening of growth expectations relative to prior projections. Nonetheless, if credit spreads are to widen materially in the months ahead, we anticipate it would be a function of sustained inflation rather than weakening credit quality, as balance sheet fundamentals and market liquidity remain strong.

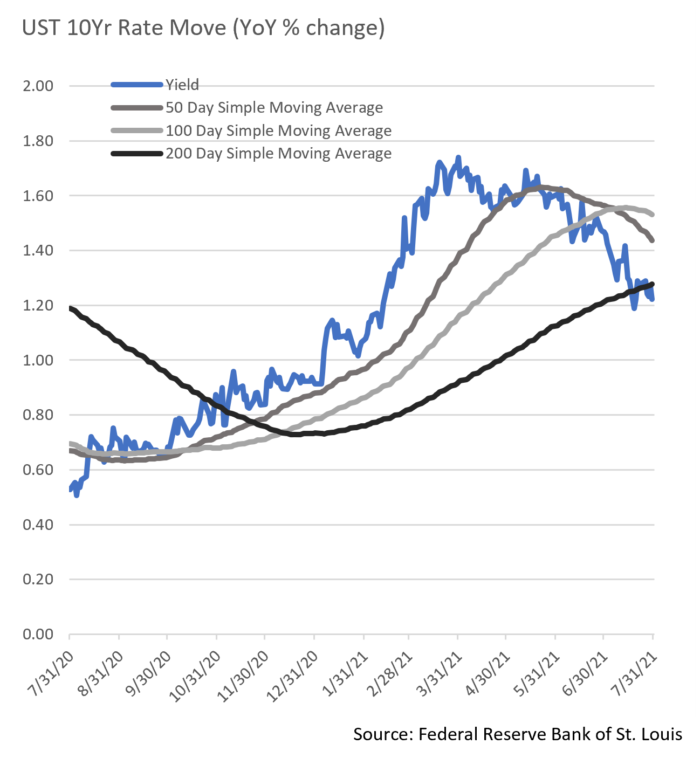

- The flattening UST yield curve theme of Q2 has spilled over into Q3. 10Yr UST yields had dropped 27 bps to 1.47% over the course of Q2, a bull flattening trend that accelerated another 25 bps in July with the 10Yr closing at 1.22%. That marked a low not seen since February and a yield level well below the 200-day average of 1.28%. This move has reemphasized the extent to which the timing and magnitude of post-pandemic economic growth remains in question, particularly with the emergence of the Delta variant. The fixed income markets are grappling with renewed uncertainty yet remain backstopped by formidable Federal Reserve and US Treasury support.

Public Sector Watch

Credit Comments

Western Weather Conditions

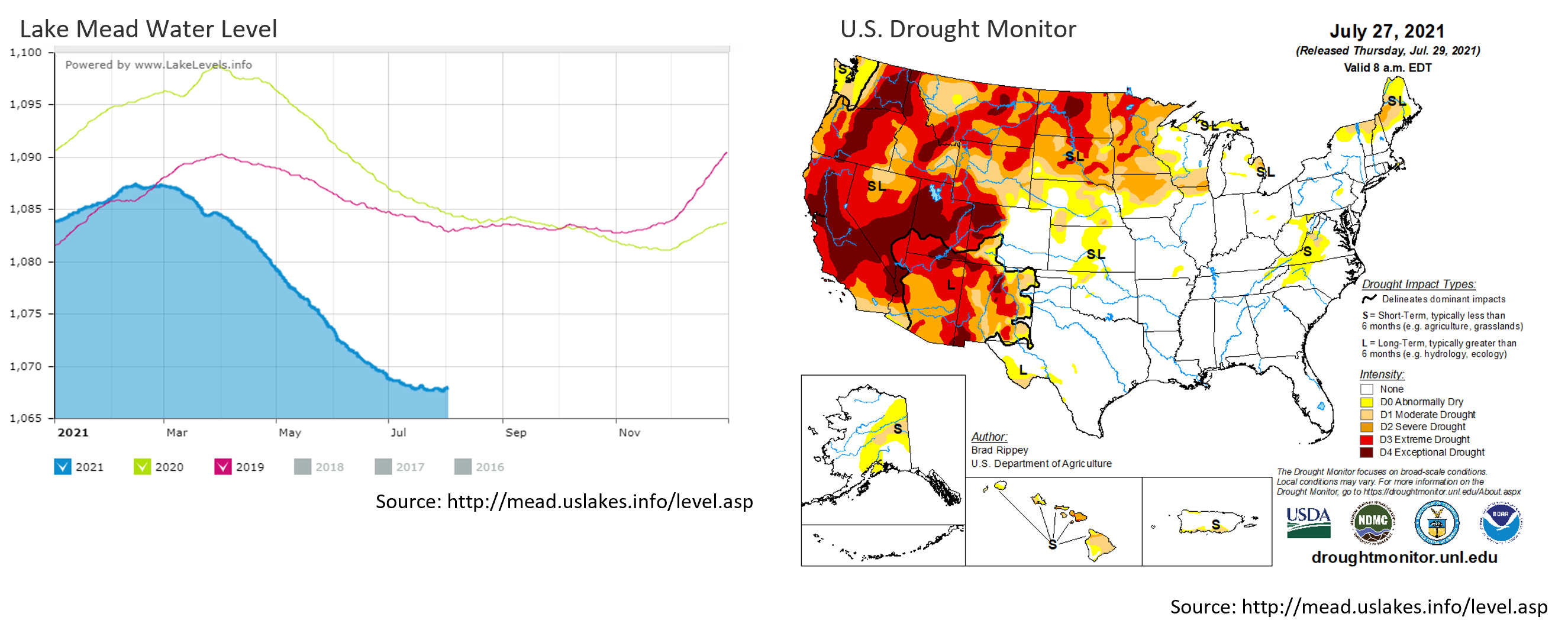

- Record-breaking drought conditions have recently impacted the Western part of the US with more than 95% of the region currently experiencing some level of drought. Nearly two-thirds of the West is dealing with extreme or exceptional drought conditions and the US Department of the Interior is highly likely to issue the first ever official water shortage declaration within the coming weeks.

- While drought conditions are not new to the West, much of which has been pursuing conservation efforts for many years, the abruptness and severity of the current drought has impacted the region. While municipal credit implications are wide-ranging, water and power shortages are expected to have the most acute effects on utility systems.

Water Systems

- 40 million people are dependent on Lake Mead and its system of aqueducts and dams for their water supply, a source that has seen decreasing water levels for two decades. Conservation has slowed the pace of depletion although these efforts have recently been outpaced by the severity of sustained drought conditions. Water levels declined to lows this year that have not been experienced since Lake Mead was filled in the 1930s.

- Conservation efforts have already impacted utility system revenues which are expected to be further reduced by the pending shortage declaration and associated usage cutbacks. Strained revenues come at a time when it is increasingly important for systems to invest in storage and water collection processes that diversify water sources. Doing so is imperative but will increase debt service and could ultimately result in lower coverage levels. Although several systems have an ability to raise rates, such increases could challenge water affordability.

Power Utilities

- Power utilities follow a similar pattern as water systems, facing supply and demand challenges amplified by intense weather patterns such as extreme heat. Severe weather increases power demand, as demonstrated by heat waves that have prompted a surge in air conditioning demand. At the same time, drought has limited hydroelectric power generation which is expected to fall 11% this year. Power grid managers have pleaded with residents to limit usage or risk rolling blackouts. Risk lies in the same feedback loop being experienced by water systems, as conservation reduces revenues at the same time costs are increasing due to efforts to diversify power sources.

- Power systems have also been affected by wildfires knocking out critical infrastructure. Most recently, the Bootleg Fire crippled the California Oregon Intertie, a key transmission system that CA depends on for electricity imports. The Bootleg Fire alone has reduced generation by 3,500 megawatts and is just one of several wildfires currently ravaging the West Coast, exacerbating a supply and demand disconnect.

The Importance of ESG and Management Analysis

- While this year’s heat and weather conditions have broken several records and appear to be an anomaly, scientists are predicting that extreme weather events such as megadroughts and 100-year storms will become increasingly common. Accordingly, Appleton’s research process incorporates current environmental conditions as well as look-forward factors we feel must be considered when evaluating climate-related risks and sustainable credit quality.

- Our credit team favors utility systems that benefit from diversified water and power sources. While this supply profile increases current expenses, it can help prevent severe weather-related events from depleting supply.

- Proactive management and ESG considerations are also very important to ensuring that effective drought mitigation and storage capacity plans are in place. Many of our approved credits have had such plans for decades.

Strategy Overview

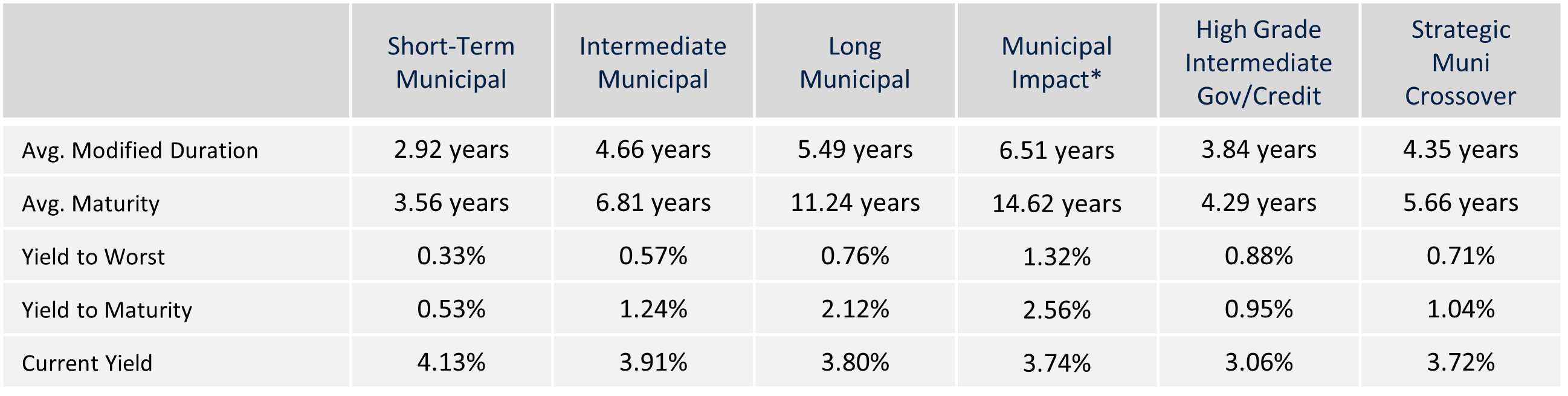

Composite Portfolio Positioning as of 7/31/21

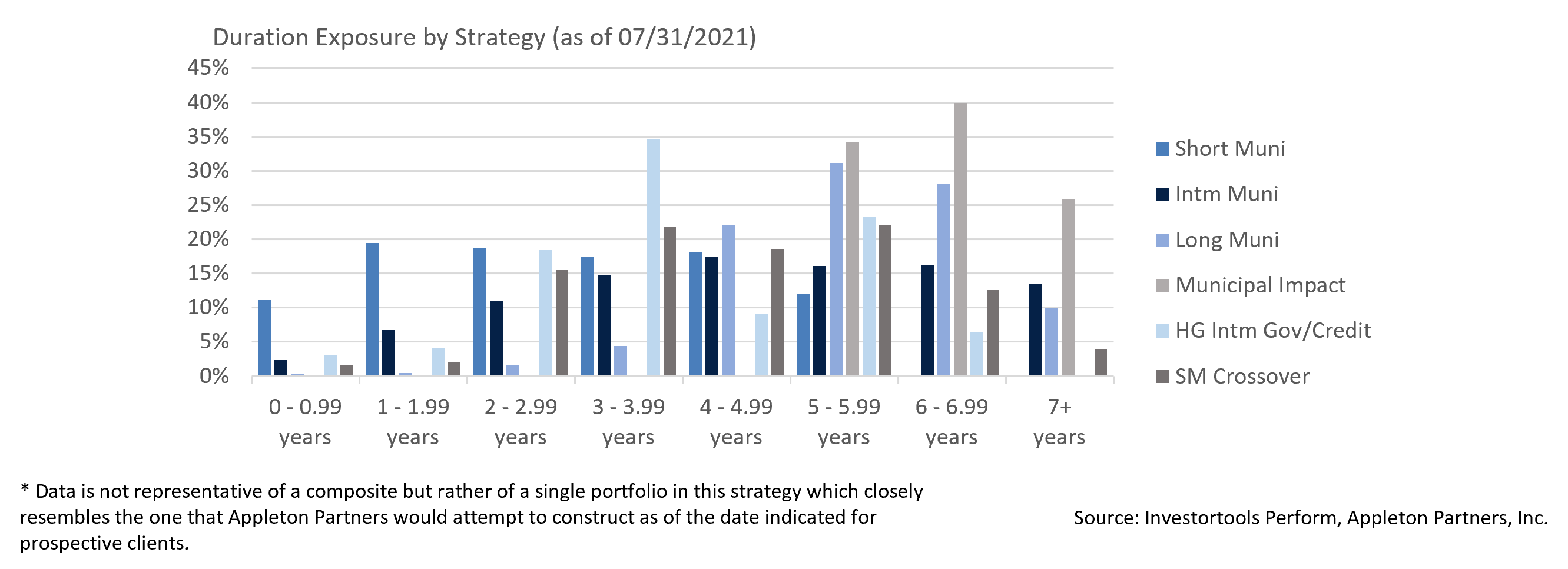

Duration Exposure by Strategy as of 7/31/21

Our Philosophy and Process

- Our objective is to preserve and grow your clients’ capital in a tax efficient manner.

- Dynamic active management and an emphasis on liquidity affords us the flexibility to react to changes in the credit, interest rate and yield curve environments.

- Dissecting the yield curve to target maturity exposure can help us capture value and capitalize on market inefficiencies as rate cycles change.

- Customized separate accounts are structured to meet your clients’ evolving tax, liquidity, risk tolerance and other unique needs.

- Intense credit research is applied within the liquid, high investment grade universe.

- Extensive fundamental, technical and economic analysis is utilized in making investment decisions.